[ad_1]

Katrina Wittkamp/DigitalVision via Getty Images

Investment Thesis

Casey’s General Stores (NASDAQ:CASY) recently announced its Q2 FY23 results. In this thesis, I will analyze the company’s quarterly results and give my opinion on its future growth potential. Their revenue is growing every quarter, and they are expanding their business by acquiring properties and opening new stores. They have put up a target of opening 80 new stores in FY23. I believe they have a bright future and excellent growth potential. So I think it is the right time to invest in CASY.

About CASY

CASY runs more than 2450 convenience stores across 16 midwestern states. They offer self-service motor fuel and a variety of food and grocery items. Their most famous food items include pizzas, donuts, and sandwiches. It also provides various products like soft drinks, sports drinks, tea, dairy products, wine, snacks, packaged bakery, electronic accessories, pet supplies, automotive products, tobacco, and nicotine products. It was founded in 1959 and headquartered in Ankeny, Iowa.

Financial Analysis

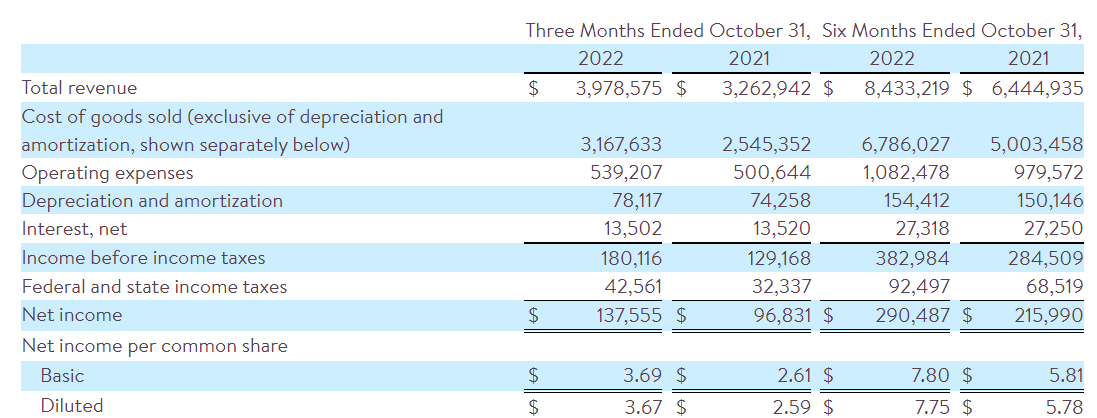

CASY recently announced its Q2 FY23 results. They beat the market EPS estimate by 19.7% and missed the market revenue estimate by 1.4%. The reported revenue for Q2 FY23 was $3.9 billion, an increase of 22% compared to Q2 FY22. I believe the primary reason behind this increase was the increase in the inside same-store sales. The sales of inside same-store in Q2 FY23 rose by 7.9% compared to the corresponding quarter of last year. Inside same-store sales include pizza and fountain sales. The reported net income for Q2 FY23 was $137.5 million, a significant increase of 42% compared to the corresponding quarter of last year. I believe there were several reasons behind this increase. The first was the total fuel gross profit increase, which increased by 22.7% in Q2 FY23 compared to Q2 FY22, and the second was the sale of general merchandise, alcoholic and non-alcoholic beverages.

Casy’s Investor Relations

The diluted EPS for Q2 FY23 was $3.67, an increase of 41.6% compared to Q2 FY22. Everything went right for the company in Q2 FY23; profit margins and adjusted EBITDA also improved compared to Q2 FY22. Overall, in my view, the financial performance of CASY in Q2 FY23 was pretty impressive, and I believe they will continue to do better in upcoming quarters; the reason they will do better I will discuss later in the report.

Technical Analysis

TradingView

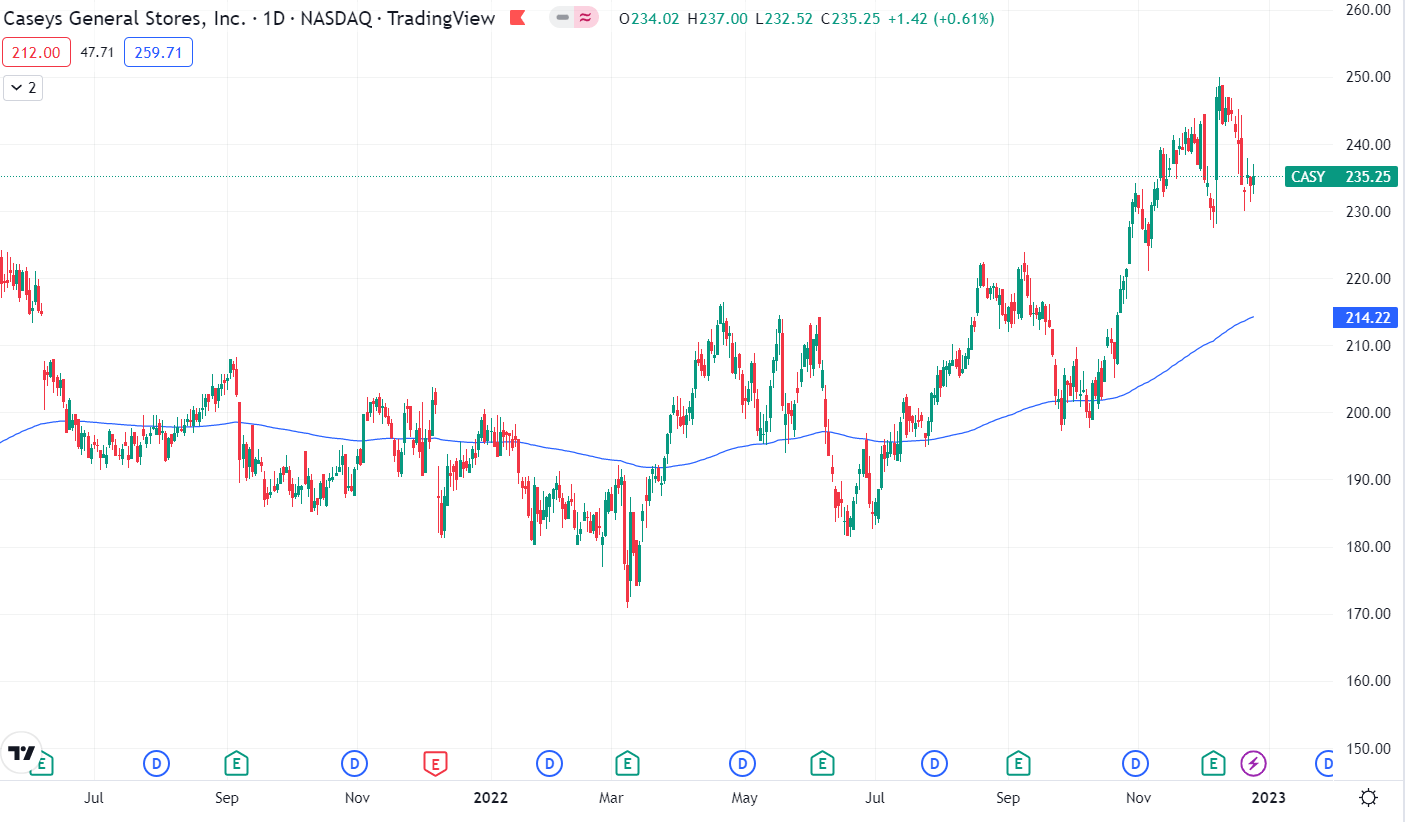

Currently, CASY is trading at the level of $235.25 and is well above its 200 ema, which is at $214.2 in a daily time frame. When a stock is trading above its 200 ema, it is considered in an uptrend. We can see that the stock is continuously forming higher highs and higher lows formation, which is regarded as a bullish pattern. Any correction in this stock will be an investment opportunity. I believe we can see a slight correction in the stock till the level of $220 because the stock has been rising continuously since last November, and a correction is mandatory. So, in my view, after the correction, one can add this stock to its portfolio. In technical analysis, there is a saying, “Ride the trend,” which applies to this stock. They are fundamentally strong and technically sound, so one should utilize the opportunity because I think it might give returns of up to 15% in the next three months.

Should One Invest In CASY?

Seeking Alpha

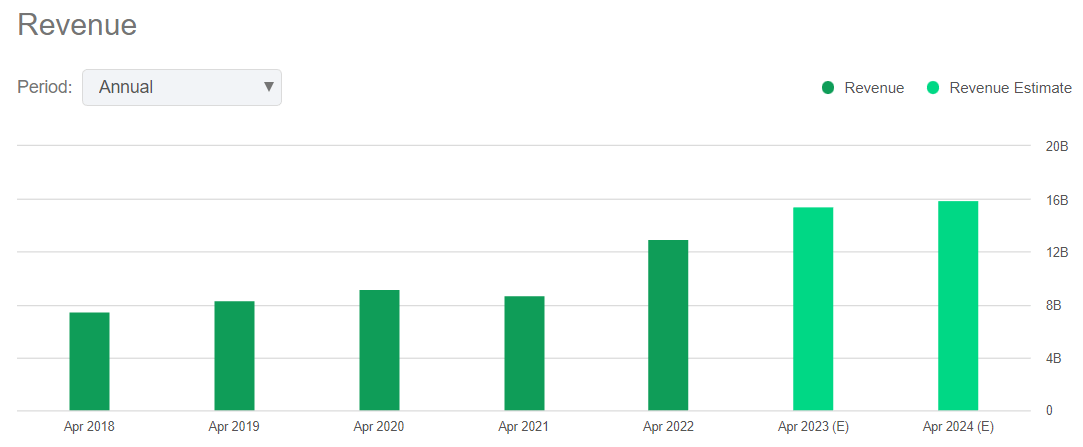

CASY performed well in FY22, their revenue grew by 48.6% compared to FY21. They have provided optimistic revenue guidance for FY23. The FY23 revenue estimate is 19.3% higher than the FY22 revenue. In the last 6 months, the company has opened 11 new stores, and it is expected to add 69 more stores by the end of FY23. Their revenues from inside same-store and fuel are constantly increasing. They have a revenue three year (CAGR) of 21.6% and diluted EPS 3 year (CAGR) of 20.4%, which shows their growth potential.

They have a P/E (FWD) ratio of 20.94x compared to the sector ratio of 19.11x. They have a Price/Sales (FWD) ratio of 0.57x compared to the sector ratio of 1.11x, which shows that they are undervalued. Generally, a Price/Sales ratio below one is considered good.

Seeking Alpha

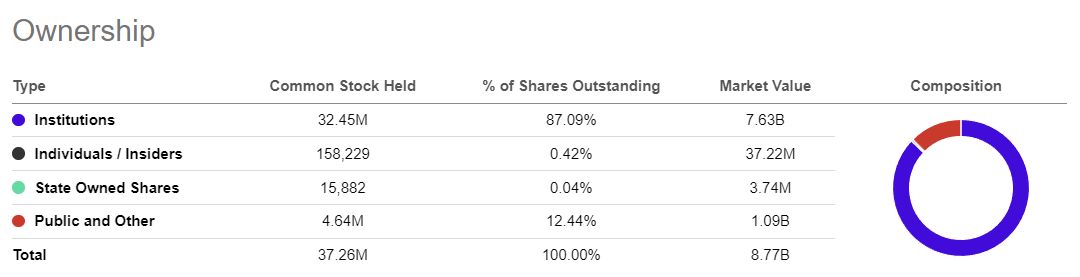

The shareholding pattern of CASY looks impressive. Institutions own 87% of the stake in the company, which is a positive sign. Where institutions own most of the stake in a company, we see less volatility in price fluctuations. This is why we see less volatility in the share price of CASY. The company is yet to purchase $400 million worth of shares under its existing share purchase program. This share purchase program shows the management’s trust in the company. The share purchase program could indicate that we can see more upside in the share price in the future.

Risk

Pandemics

Lockdown due to the Covid pandemic severely impacted their business, and with covid rising again in the Asian region can be a matter of concern. Another pandemic or a disease outbreak may lead to decreased store traffic and problems in its supply chains, like difficulty with delivering products in its stores. Their business runs through their physical stores; they don’t do online business, so if the government imposes a lockdown or a riot-like situation arises, they might have to close their stores. It can severely impact the business and balance sheet of the company.

Bottom Line

I believe CASY is a high-growth and promising company. Their revenues are growing rapidly, and their store network is also increasing every quarter, which is a positive sign. I am optimistic about their future growth. They are fundamentally strong and also look strong in the technical charts. So after analyzing all the aspects, I am long on CASY.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.