[ad_1]

sarawuth702

Electric Vehicle EV maker Rivian (NASDAQ:RIVN) came public recently with much fanfare; however, it ended up being just that – all sizzle and no steak. The Macro backdrop is working against the company in 2023, and there is the beginning of an energy crisis forming (energy may be volatile, and expensive this winter). Also, there are a number of smaller competitors in the space that offer more value if one wants to enter into the once hot EV market.

Fundamentals

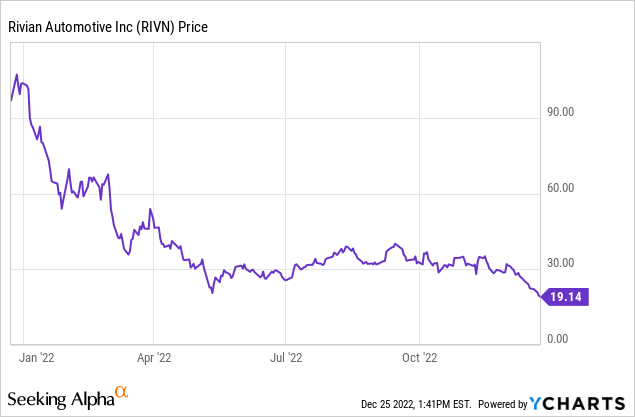

Rivian is now $18 Bn valuation but it was once much higher. The company’s stock is now trading at $19/share but it was once over $100. Check out the chart:

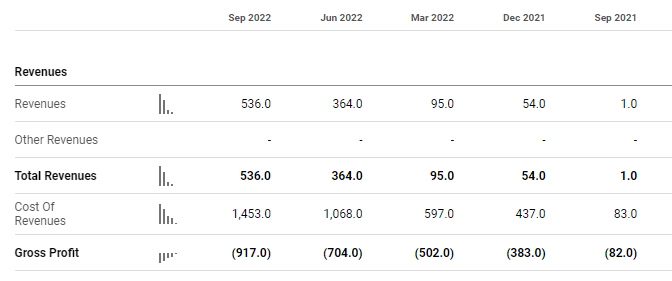

The broader market has sold off this year, to be fair. But Rivian has other reasons for the sell off. After the IPO, the Amazon deal fell apart, and then things seemed to continue to fall apart at the seams. Rivian is a great company but the question is what is the company worth, in valuation? That is the million dollar question on everyone’s mind. Rivian has a growing loss, look at the most recent financial statement:

Seeking Alpha

Total Revenues are growing, but so is the Cost of Revenues. Is the plan to simply grow by merger, acquisition, and through big partnerships like the one with Amazon? That’s not a bad strategy, but investors are counting on third parties to strike a deal, which is a huge unknown. The Amazon failure is proof that it’s unwise to rely on third parties.

We don’t see a clear path for Rivian to get out of the hole they are in. In other words, if we extrapolate the current linear results into the future, we will just see a bigger hole getting bigger. Based on this it’s hard to say what the true value might be, and we aren’t suggesting one – just that it is likely lower.

Valuation

For valuation assumptions we are typically looking at the Price to Earnings ratio or P/E ratio, but that doesn’t work if the company isn’t turning a profit. When a company is running a negative P/E investors are 100% exclusively betting on future performance. Let’s just take a quick look at a traditional car company, Ford (F) which has a market cap of about $45 Bn and total Revenues of about $40 Bn, and a P/E of about 5.75 as of this writing. Yes, it’s hard to compare with well established companies but that’s exactly our point. Where and how do you draw the valuation line for a startup like Rivian in a new sector, Electric Vehicles. We all know the metrics how to value companies like Ford who have been around for a very long time.

Unfortunately, it is our opinion that many investors are using the Tesla model in order to value other EV companies which is not applicable or appropriate. In fact, our opinion is not only Rivian is overvalued, but the whole sector (excluding some of the micro caps out there which are undervalued).

Competitors

Rivian has many competitors as the EV market is a new market. One could say that any EV maker is a competitor, so we’ll list a few that make similar models of vehicles, and exclude Tesla (TSLA) because Tesla has the first mover advantage. Competitors include Workhorse (WKHS), Nikola (NKLA), Arrival (ARVL), GreenPower (GP), ELMS (OTC:ELMSQ), Cenntro (CENN), and Mullen (MULN).

Out of these, we like Mullen and Cenntro. The reason is simple, they are micro-caps with more room to move up, and have solid growth prospects. We don’t think that necessarily Rivian is going to be displaced by a competitor, because the EV market is huge and there is simply not enough manufacturing to keep up pace with demand – all new players are welcome. However, we have to compare apples to oranges here, because there’s a lot of room for competitors like Cenntro and Mullen to move up, whereas it would take a huge deal to move the needle on Rivian.

Cenntro Auto is a Chinese manufacturer with a strong presence in the USA (Freehold, NJ) and in the EU (Germany). Mullen is a US-founded group that makes a similar line of EV cars, and has a strong reputation. There are many, many others – and that’s the point.

Rivian is going to have to convince the market they are better than all these up and coming companies.

EV Market

The total EV market is huge, in 2021 it was nearly $200 Bn and expected to grow over a Trillion by 2030. There is no question that Rivian has contributed to the positive development of a new industry, and it’s a big one. The question is how much should Rivian be valued at given the current set of circumstances.

EV is not just about saving the planet, it’s about economic sustainability. This past week there have been power outages and rolling blackouts across USA, making the entire infrastructure work. An EV that’s powered by Solar or other off-grid electricity would not be subject to such disruptions. We believe EV has a great future and we are not against Rivian as a company, just that the stock has been pumped up with a lot of sizzle and no steak to follow.

Conclusion

Because we feel Rivian is overvalued, we would sell here. We are not suggesting short selling, Rivian has a real business and it should be OK in the long run, given how important the EV market is. We do not agree with non-organic business growth, we believe that real growth comes from sales, not partnerships. Sales and predictable revenue streams are the keys to success, the keys to the kingdom. If you don’t own any Rivian, check out another EV company. If you own it, we would sell it and rotate the funds into something else.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.