[ad_1]

Dzmitry Dzemidovich

Ellington Residential Mortgage REIT (NYSE:EARN) was one of the few mortgage trusts I purchased in 2022, and I only did so after the company reduced its dividend payout by 20% to $0.08 per share.

Mortgage trusts, including Ellington Residential, took significant valuation hits in 2022, and 2023 is likely to be a difficult year for the sector as interest rates rise.

Having said that, Ellington Residential and other mortgage trusts could fall even further as the Fed is expected to raise the benchmark federal funds rate above 5% in 2023.

I believe the trust is a potentially appealing addition to a passive income-tilted portfolio, but I’d wait until a bottom has been identified.

Steeping Yield Curve Represents A Big Risk For the Mortgage Trust Sector

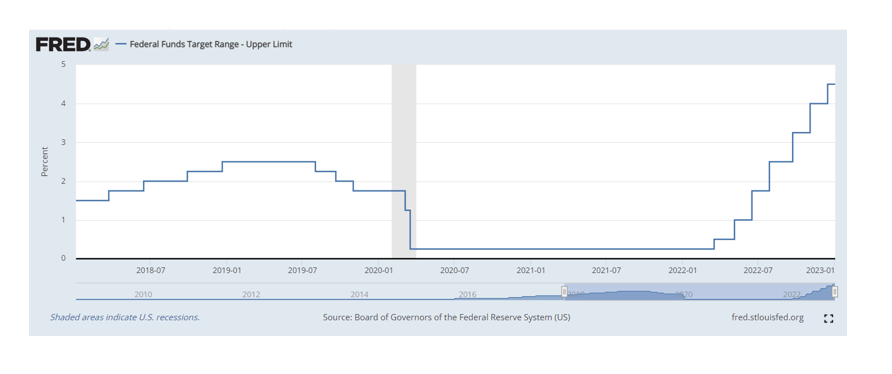

Few, if any, investors correctly predicted how quickly the Fed would raise interest rates in 2022. The Fed ended the year with a benchmark federal funds target range of 4.25-4.50%, and with inflation remaining subdued, it could rise above 5.0% as early as 1Q-23.

The central bank has raised rates at a rate not seen in the market in over a decade and a half, and the steepening of the yield curve is a major challenge for the mortgage trust sector because it represents higher funding costs and pressure on the net interest spread on which mortgage trusts rely.

Federal Funds Target Range (Fred.stlouisfed.org)

Mortgage trusts, such as Ellington Residential, rely on a lot of short-term financing to buy mortgage securities with high yields. If funding costs rise, as they did in 2022, mortgage trusts lose money and see their portfolio values fall.

Ellington Residential reported a book value of $7.78 per share at the end of the September quarter, implying that the trust’s book value fell by 33.8% from January to November.

Other mortgage trusts, such as Annaly Capital Management, Inc. (NLY), have seen dramatic declines in book value in 2022, primarily as a result of mortgage-backed security spreads widening.

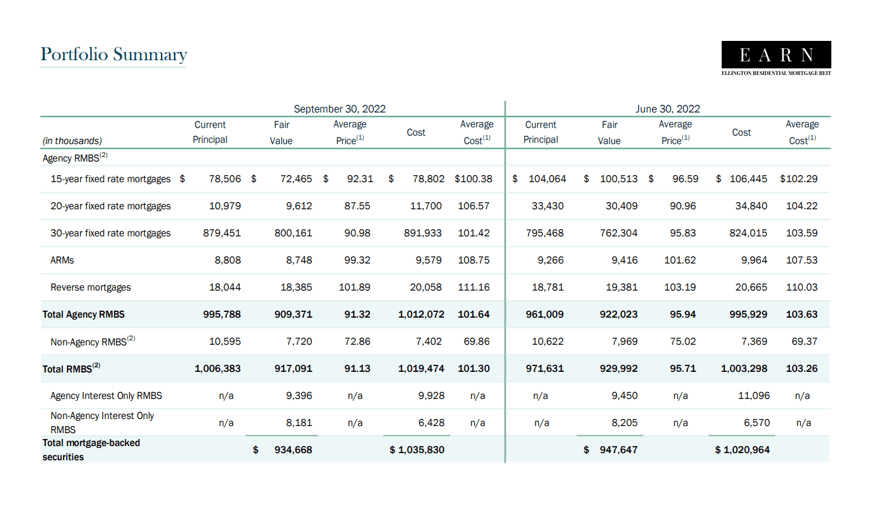

Ellington Residential’s total portfolio value fell 28.7% to $934.7 million from the end of 2021 to the end of 2022. The trust primarily invests in residential mortgage-backed securities, the value of which has declined as a result of the central bank’s actions.

Moving forward, the pressure on mortgage trust portfolio value may ease if inflation falls and the market sees signs of Jerome Powell’s more dovish interest rate policy.

Portfolio Summary (Ellington Residential Mortgage REIT)

Trading At A Discount Valuation

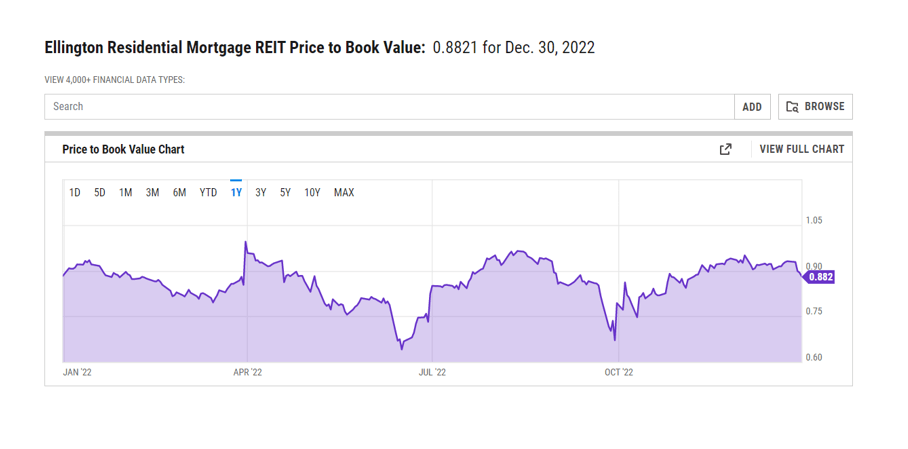

The central bank’s actions have caused a lot of turmoil in the market for mortgage-backed securities in 2022, resulting in a lot of mortgage trusts now selling at discounts to book value.

Ellington Residential’s stock is currently trading at a 12% discount to book value, but there is a good chance that the book discount will widen again in 2023 if the Fed decides that simmering inflation remains a top justification for more jumbo-sized interest rate hikes in 2023.

Price To Book Value (YCharts)

Wait For A Bottom Before Grabbing EARN’s 14% Yield

I purchased Ellington Residential shortly after the trust cut its dividend payout by 20% last year, from $0.10 per share to $0.08 per share.

Ellington Residential stock currently pays a 14% yield based on the current dividend payout, and the high yield, in my opinion, reflects above-average dividend risks. Before buying EARN, I believe investors should wait until it has reached a bottom.

Why Ellington Residential Could See A Lower Valuation

An acceleration in inflation rates in 2023 may tempt the Fed to step back on interest rate hikes, resulting in an even steeper yield curve, higher interest costs for mortgage trusts that deal with a lot of short-term financing, and ongoing pressure on Ellington Residential’s portfolio value.

If inflation eases and interest rates begin to fall again in 2023, mortgage trusts such as Ellington Residential could be attractive dividend investments.

My Conclusion

Before purchasing Ellington Residential’s 14% dividend yield, I believe passive income investors should wait for a bottom.

The stock has most likely not reached its lows, and the trust’s portfolio value may face ongoing pressure as the central bank’s interest rate policy remains a wild card in 2023.

Even though the stock is already trading at a discount to book value, if the interest rate curve continues to steepen in 2023, the market will punish Ellington Residential with an even greater discount to book value.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.