[ad_1]

Dilok Klaisataporn

With many banks offering competitive rates on CDs, one may wonder why dividend paying stocks should remain attractive. For one thing, the rate of return on a CD is near guaranteed, supposing that the saver keeps a balance under the FDIC threshold.

Drawbacks to CDs, however, include the limited term for their rate of return. There is no guarantee that the saver will be able to rollover their funds at the same or higher rate when the CD matures. That’s why I’d rather put money to work in quality dividend paying stocks that have a track record of raising their distributions.

One such segment is utilities, many of which carry bond-like qualities for their regulated revenue streams. Such I find the case to be with Duke Energy (NYSE:DUK). This article highlights what makes DUK a worthy candidate for an income portfolio at the right price, so let’s get started.

Why DUK?

Duke Energy is one of the largest regulated utility companies in the U.S., with a presence in 6 states covering over 7 million customers. The company operates in the three primary segments of electric utilities and infrastructure, gas utilities and infrastructure, and commercial renewables. Its regulated utilities provide a stable and predictable earnings stream, which allows the company to make long-term investments and plan for future growth.

Duke Energy is evolving as it’s investing in the modernization of its grid infrastructure, which will enable it to better serve the needs of its customers and to capitalize on the growing demand for clean energy. This includes the deployment of smart grid technologies, such as advanced metering and distribution automation, which will improve the efficiency and reliability of the company’s electric grid.

Moreover, management plans to exit those businesses with slower EPS growth than its utility platform, and thereby transform itself into a pure-play utility. This is supported by management’s plans to sell its commercial renewable energy business, which represents around 5% of DUK’s total earnings, leaving the rest of the business as a fully regulated utility.

Proceeds from a sale will help to fund DUK’s $145 billion capital plan across higher growth regulated electric and gas operations, and targets of 5% to 7% annual EPS growth through 2027. In the near term (through 2027) management expects around $65 billion worth of investments in clean energy, and the remaining $80 to $85 billion to be spent post 2027 to support future rate base growth.

Meanwhile, DUK’s core operations are doing well, with growth in the electric utilities and infrastructure segment driven by higher retail electric volumes and lower operations and maintenance costs during the third quarter. Its gas utilities business is also performing well with higher riders and rate case contributions.

Looking forward, DUK stands to benefit from proactive legislation in North Carolina around rate cases, which enables line of sight for capital projects around clean energy. This was highlighted by Morningstar in its recent analyst report:

In North Carolina, Duke’s largest service territory, recent state legislation includes numerous provisions that significantly improve the state’s regulatory ratemaking structure. The legislation allows multiyear rate plans up to three years, including increases for projected capital investments.

Duke expects to file rate cases at both state subsidiaries later this year and early next year. Additionally, it allows for performance incentive mechanisms and usage-decoupled rates for residential customers, protecting utilities from underlying usage trends. The legislation also supports utilities playing a critical role in the state’s clean energy transition.

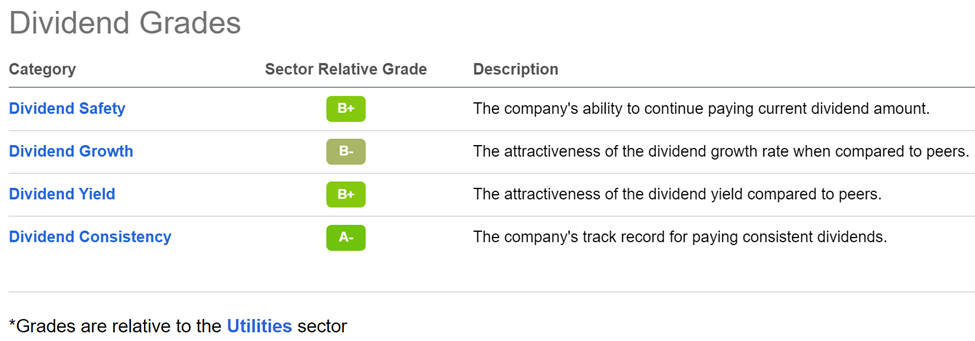

Importantly, DUK maintains a strong BBB+ rated balance sheet to support its clean energy transition. It also pays a 3.8% dividend yield that’s covered by a 77% payout ratio and 11 years of consecutive dividend growth. While DUK’s 5-year dividend CAGR is just 2.7%, that could change in the future as management targets a 5% to 7% annual EPS growth rate. As shown below, DUK carries A and B grades for dividend safety, growth, yield, and consistency.

DUK Dividend Grades (Seeking Alpha)

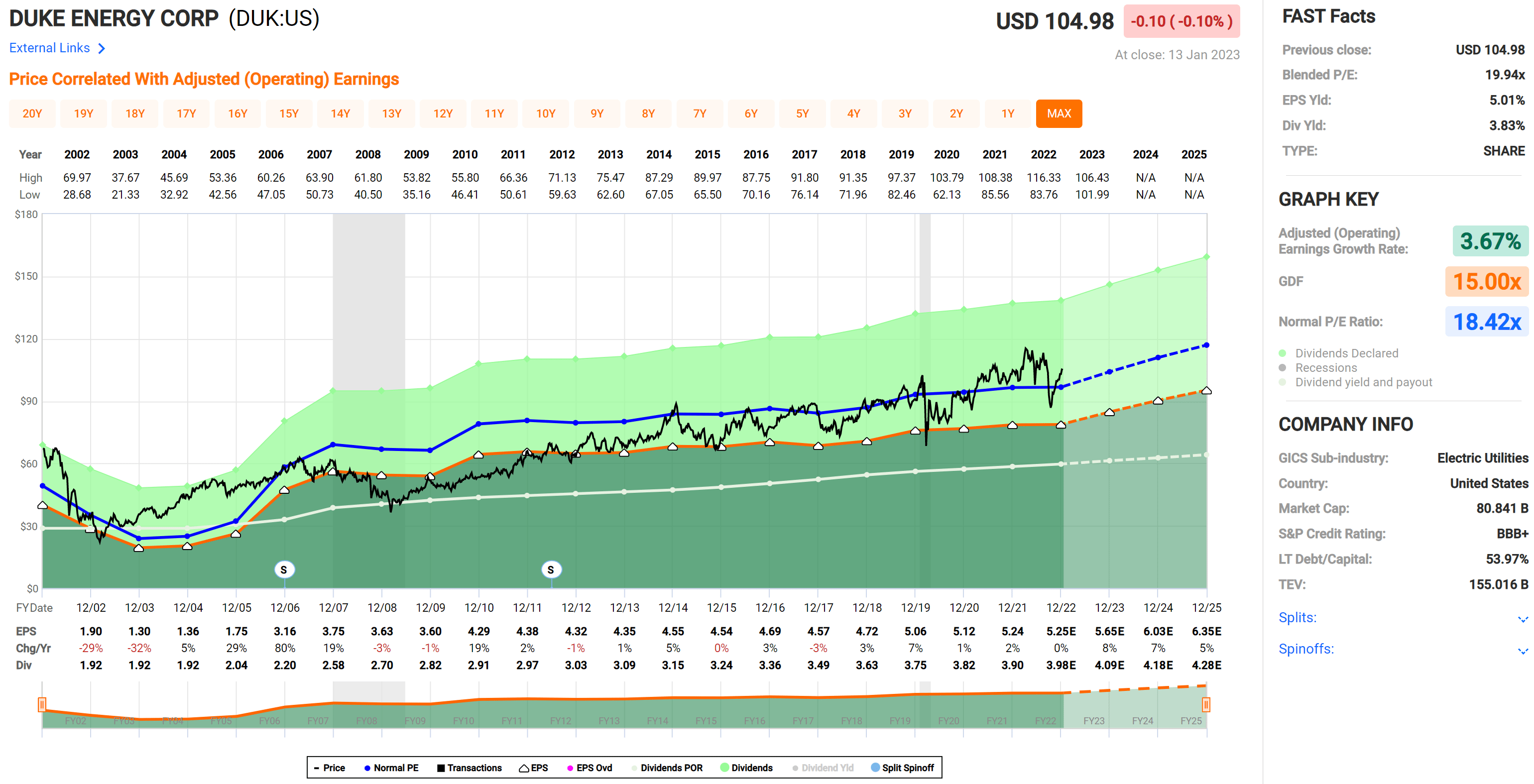

Turning to valuation, I find DUK to be soundly valued at the current price of $104 with a forward PE of 19.6, sitting above its normal PE of 18.4. Moreover, if we apply an expectation of 10% annual returns, then we would need at least a 4% dividend yield plus the 6% average EPS growth rate that management expects going forward. This translates to a price target of $100 or less. For an added margin of safety, I would target an entry price of $95 or less.

DUK Valuation (FAST Graphs)

Investor Takeaway

Duke Energy is an attractive utility stock trading at a fair price and is in the process of transforming itself into a pure-play regulated utility. The company’s capital investments in modernization of its grid infrastructure and clean energy assets, as well as proactive legislation in North Carolina, should drive higher earnings growth going forward. Meanwhile, I find DUK to be fairly valued at present and would recommend waiting for a pullback in price before buying this great utility company.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.