[ad_1]

cagkansayin

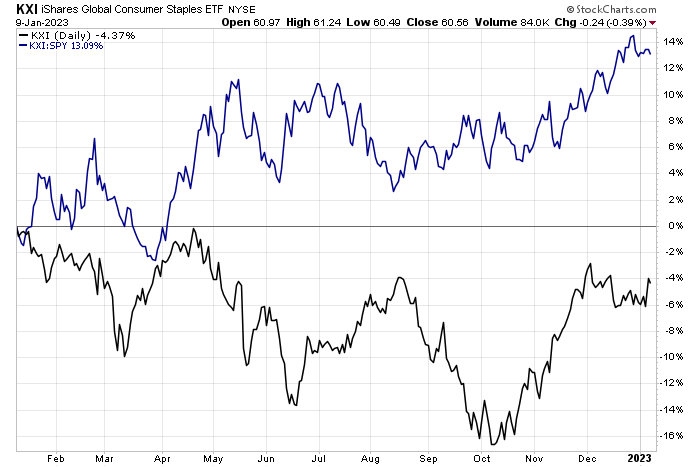

Consumer Staples stocks continue to fetch a valuation premium in this uncertain market. Also, a sudden lovefest with foreign equities has helped send both ex-US developed and emerging markets up close to 20% from their Q4 2022 lows, easily beating the return on the S&P 500. One under-the-radar ETF holds staples stocks around the world.

The iShares Global Consumer Staples ETF is down just 4% total return over the last year, outpacing the S&P 500 by more than 13 percentage points. One firm has caught a bid in the last 12 months, but shares remain stuck in a downtrend. But is Ambev a buy now on valuation? Let’s check it out.

Global Staples Rally Hard Since October

StockCharts.com

According to Bank of America Global Research, AmBev S.A. (NYSE:ABEV) is the world’s fourth-largest brewer and the largest Pepsi bottler outside the US. Beer brands Skol, Brahma, and Antarctica have a nearly 67% share of the Brazilian beer market by volume. The company also has operations in Canada via Labatt and is present in several South and Central American countries. AmBev is controlled by Anheuser-Busch InBev (BUD).

The Brazil-based $46.7 billion market cap beverages industry company within the Consumer Staples sector trades at a near-market trailing 12-month GAAP price-to-earnings ratio of 17.3 while it pays a high 4.0% dividend yield, according to The Wall Street Journal. Despite hopes that positive sales related to exposure from the 2022 World Cup, shares have been generally on the move lower in the past two months.

Before the global sporting event, ABEV reported Q3 earnings that were positive, along with a solid 11.4% annual jump in revenues. Shares managed to stage a short-lived rally after that earnings announcement. Near term, political unrest in Brazil could be pressuring the stock, but it is off lows notched to kick off 2023. High uncertainty and tough comps are key risks for 2023 sales and earnings, but lower commodity prices could help the firm.

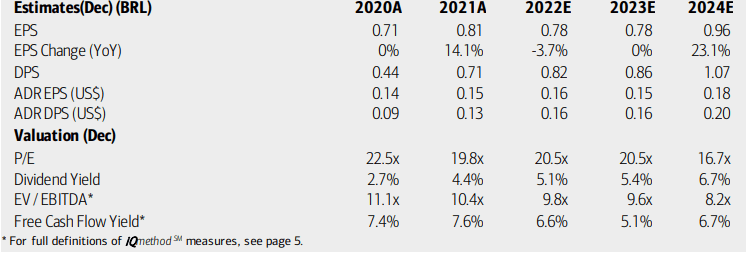

On valuation, analysts at BofA see earnings having fallen slightly in 2022 before flat-lining next year. Per-share profits are expected to rise notably in 2024, though. Dividends are seen as rising at a steadier pace than EPS. Still, the P/E ratio of Ambev does not scream cheap, but the EV/EBITDA ratio is significantly below that of the typical S&P 500 stock.

The alcohol company generates free cash flow, which is a positive. Overall, the valuation seems decent, but not extremely attractive here considering lukewarm growth. The resulting PEG ratio is near 2 while the price-to-sales multiple is almost 3.

Ambev: Earnings, Valuation, Dividend Forecasts

BofA Global Research

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2022 earnings date of Thursday, March 2 BMO. A shareholder meeting takes place in late April while a near-term volatility catalyst could strike when Ambev’s management team speaks at the 2023 Latin America Investment Conference (Jan 31-Feb 1).

Corporate Event Calendar

Wall Street Horizon

The Technical Take

With a lukewarm valuation and geopolitical jitters, what does the chart say above ABEV? I decided to take a long-term view of the chart. Notice below that ABEV remains well off its all-time high, notched back in 2012. In fact, a steep downtrend is in play off the early 2018 peak, when many non-US firms topped out.

Interestingly, the stock made an attempt to rise above that trendline during Q4 last year, but the rally fizzled. Even if shares break above it, there’s further resistance in the $3.75 to $4 range – the early 2016 and 2019 lows, along with that price spot being resistance during mid-2021. I see modest support around $2.40. Overall, the current consolidation looks more like a pause in the trend of a larger degree (down) but a move above $4 would help support the case that a bottom is in.

ABEV: Waiting For A Break In Trend

StockCharts.com

The Bottom Line

With earnings uncertainty this year, a market multiple (though a high yield and positive free cash flow), and a lackluster chart, I would avoid ABEV for now. It is not a hard sell, but there are better trends in US and non-US staples stocks.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.