[ad_1]

Darren415

This article was first released to Systematic Income subscribers and free trials on Dec. 16.

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company (“BDC”) sector from both the bottom-up – highlighting individual news and events – as well as the top-down – providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the third week of December.

Be sure to check out our other Weeklies – covering the Closed-End Fund (“CEF”) as well as the preferreds/baby bond markets for perspectives across the broader income space. Also, have a look at our primer of the BDC sector, with a focus on how it compares to credit CEFs.

This will be our last BDC Weekly this year. Happy holidays to our readers!

Market Action

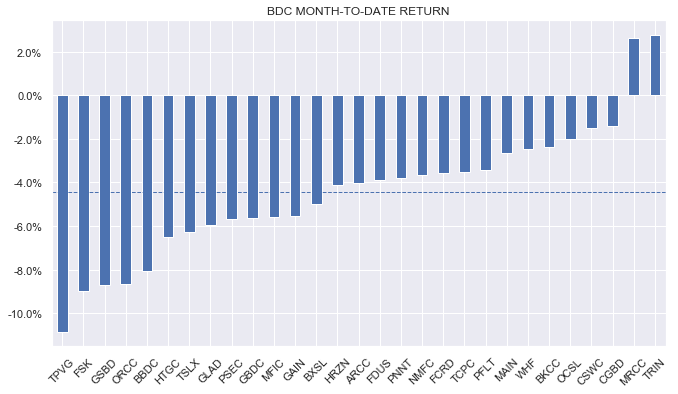

BDCs underperformed once again this week, falling around 2%. Month-to-date, the sector is down a bit over 4% with TRIN in the lead due to its recent dividend hike as we discuss below.

Systematic Income

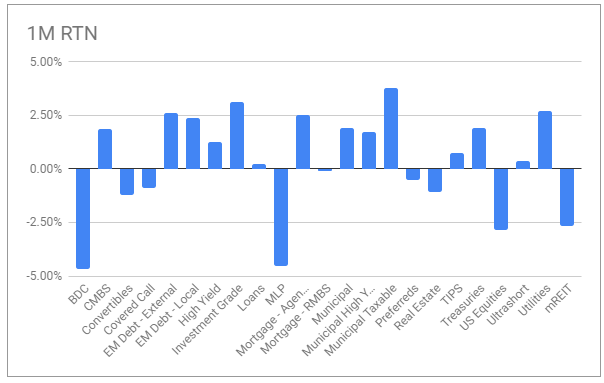

BDCs have been underperforming the broader income sector for about a month now despite resilient short-term rates and continued drip of steady dividend hikes. Over this period the sector has lacked the support of falling Treasury yields which have helped longer-duration sectors. In contrast, BDCs have behaved much like other higher-beta equity income sectors such as MLPs and mortgage REITs, among others.

Systematic Income

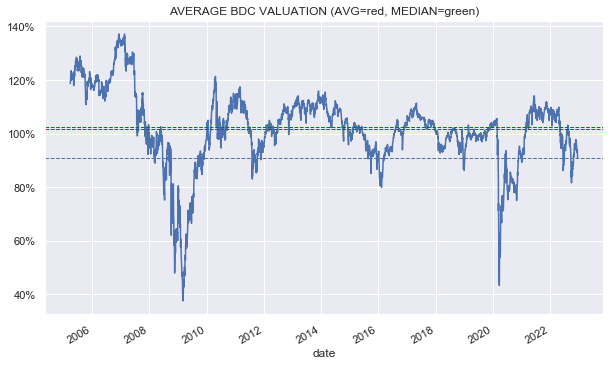

The average sector valuation has continued to fall and now stands at 91%. As we have highlighted a number of times, a valuation in the high 90s that we saw recently was clearly excessive for the sector given potential macro clouds on the horizon. The sector is now fairly-valued in our view.

Systematic Income

Market Themes

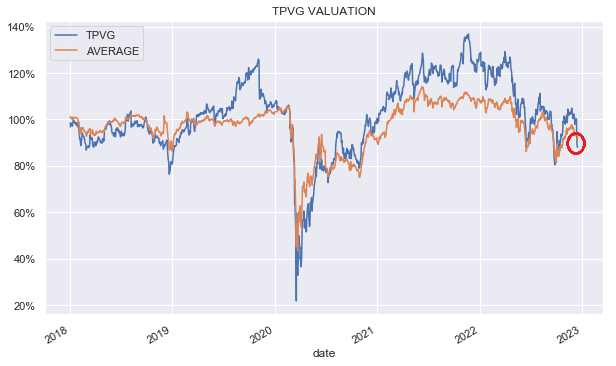

TriplePoint Venture Growth (TPVG) underperformed this week on the bankruptcy news of one of its holdings – Medly Health. The holding was marked around 93% in September which seems high given this news. We don’t know where the actual realized loss will come out but it could shave off a couple of percent off the NAV. The loan itself is worth about 7% of the NAV.

This recent move has caused the company’s valuation (based on an arguably overstated Q3 NAV) to dip below the sector average after trading above the sector average for a couple of years.

Systematic Income

Interestingly, TPVG used to trade cheaper than the sector up to around the second half of 2019 during the period when it outperformed the sector. At that point it began to mostly trade at a premium versus the sector – at one point reaching a peak of 25% above the sector valuation. However, just when its valuation moved to trade above the sector average it started to underperform the sector – a pattern we see fairly often.

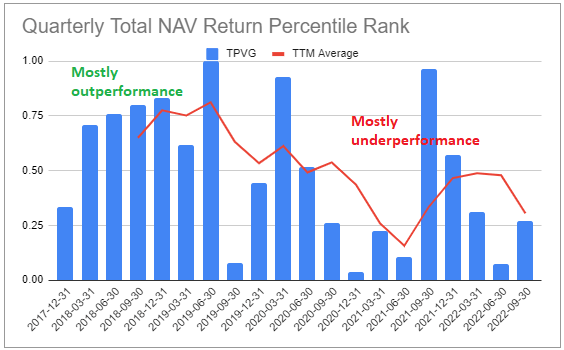

Its performance relative to the sector can be easily seen in the following chart which plots the quarterly total NAV return percentile of TPVG – a figure of 0.5 indicates median performance. The red line is a twelve-month average and clearly shows the performance of the stock gradually moved lower over the last 5 years even as its valuation grew more expensive relative to the sector. In other words, the stock’s high valuation through 2021 was running on the fumes of its pre-2019 outperformance and did not reflect its actual performance at the time.

Systematic Income BDC Tool

It seems like it took this bankruptcy to push the valuation back below the sector average which is certainly odd since its recent couple of years of underperformance is clearly out there. It is curious why the market often behaves like a coyote running off a cliff in this regard but it’s good to take advantage of, particularly in the opposite direction.

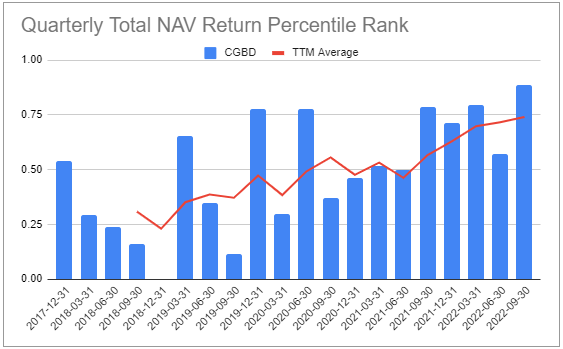

For example, Carlyle Secured Lending (CGBD) has been outperforming the sector for a couple of years now but its below-average valuation is still tied to its subpar performance from 5 years ago. We continue to hold CGBD and avoid TPVG in our Income Portfolios.

Systematic Income BDC Tool

Market Commentary

Trinity Capital (TRIN) increased its base dividend from $0.45 to $0.46, keeping its $0.15 supplemental the same for the 4th quarter. The sum is higher than the Q3 net income of $0.56 so they are likely baking in further increases in income for Q4 – not a bad sign. We moved the stock to Hold from Buy – there is clearly a lot of noise around the mining market as well as the broader crypto universe which is likely to keep some pressure on the stock despite its low allocation to the sector and its cheap valuation. It’s trading close to a 22% yield.

TCP Capital Corp (TCPC) declared a $0.05 special dividend which is about 16% of its $0.32 base dividend. The company increased its base dividend in Q3 from $0.30 however as discussed in the last article even that hike was a massive $0.10 below its level of net income. With portfolio quality stable it was inevitable that we would see a further increase in the base dividend or a special. We suspect they will increase the base dividend once again in the next quarter – their approach to dividends looks unnecessarily cautious.

Stance And Takeaways

In closing out the year of our BDC commentary, we continue to see value in higher-quality BDCs such as (BXSL) and (GBDC) which are also trading below the sector average valuation, providing additional margin of safety for investors. Both BDCs have weathered the first three quarters of the year very well, outperforming the sector in total NAV terms, and have both hiked their base dividends. They are trading at 10.6% and 10.2% yields respectively.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.