[ad_1]

Andrzej Rostek

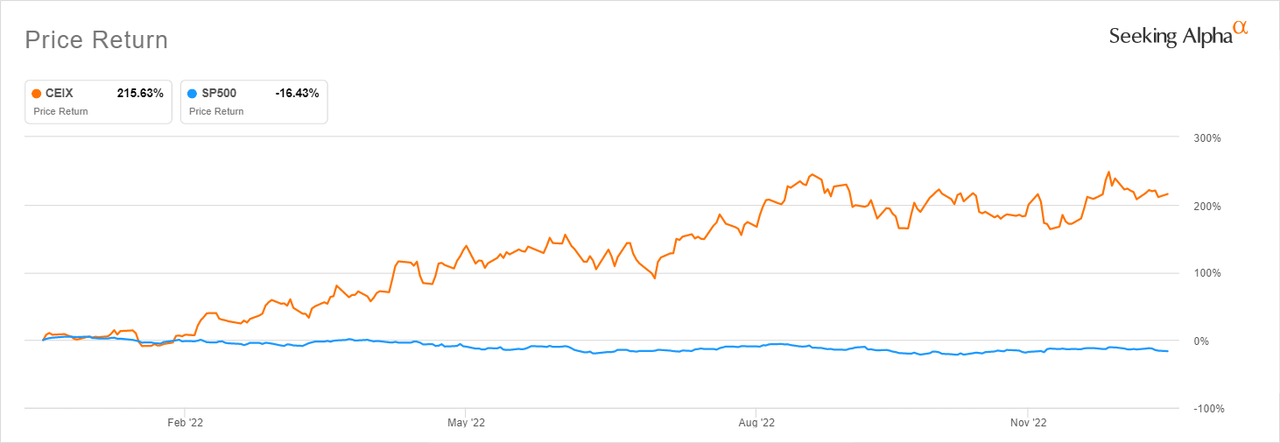

CONSOL Energy Inc. (NYSE:CEIX), a major U.S. coal producer and exporter, is up an impressive 202% YTD. This makes it one of the best-performing stocks in a year when the broader market, represented by the S&P 500 (SP500), has contracted by double digits.

CEIX YTD performance vs S&P 500 (Seeking Alpha)

The main catalyst for CEIX’s spectacular performance is the unprecedented surge in the price of coal, which has improved coal producers’ earnings and led to the increase in the stock prices of stocks in the industry.

Coal’s price has increased substantially in 2022 on huge growth in demand amid constrained supply brought on by the global push by governments and ESG investors to limit investments in the industry and accelerate the transition to clean energy.

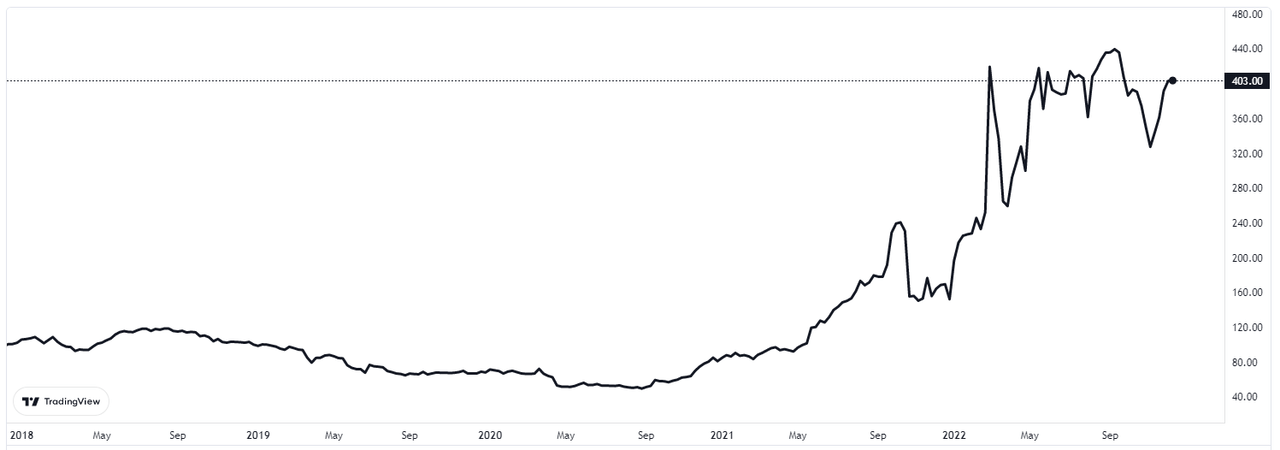

According to the International Energy Agency, coal consumption in 2022 will surpass the annual record set in 2013, and coal demand is likely to increase further in 2023 to a new all-time high. These expectations are reflected in the current price of the commodity. Newcastle Coal Futures, one of the key benchmarks, shows that coal is currently trading at around $400 per tonne. Never has coal been this expensive.

Coal 5 year price chart (Trading View)

CEIX has benefited from stronger pricing for coal as the commodity’s high price has enabled it to supercharge its revenue growth in 2022. This has boosted its free cash flow and improved its net income position.

Strong results

CEIX operates three underground coal mines in the Pennsylvania Mining Complex (PAMC). These are the Bailey, Enlow Fork and Harvey mines. The company also operates a coal export terminal in Baltimore Maryland. It exports its own coal and third party coal via this terminal.

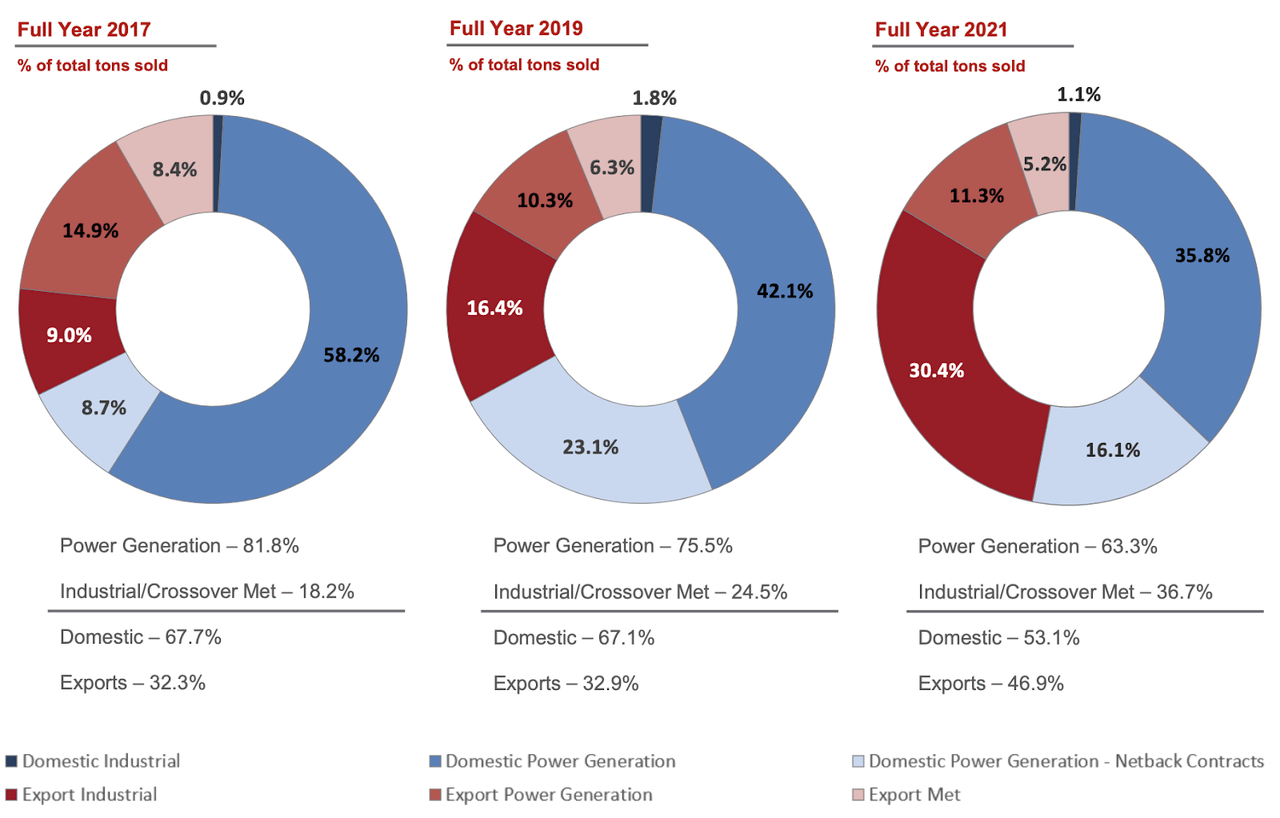

CEIX is well diversified in terms of its customer base. It serves both domestic and export markets and also produces the two main types of black coal products – thermal and metallurgical coal. Thermal coal (also called steaming coal) is used for electricity production. Metallurgical coal (also called met coal or coking coal) is used for steel making and other industrial processes.

Product and market mix (CONSOL Energy)

While CEIX’s production volume has remained relatively flat in 2022 – with a full year production guidance of 23.75 million tons to 24.50 million tons compared with the 2021 annual production of 23.9 million tons – revenue has increased substantially thanks to the astronomical increase in the price of coal.

The company is expected to report revenues of $1.98 billion in 2022, a 55% jump from $1.27 billion in 2021. Other key financial metrics, including cash flow, net income and EPS, have been trending favorably as a result of this strong topline growth.

For the most recently reported Q3, the company had a net income of $152.1 million that resulted in record EPS of $4.27. Net cash provided by operating activities came in at $153.1 million and quarterly free cash flow came in at $107.1 million.

The cash windfall in 2022 has enabled CEIX to aggressively pay down its debt. “We have now made total debt repayments of $211 million in the first three quarters of 2022 and our current gross debt level now sits at just above $450 million,” noted the company’s CFO Mitesh Thakkar on the Q3 earnings call. The goal is to continue deleveraging until debt levels reach $300 million. CEIX has also started paying dividends in light of the record cash generation. It paid $1.05 per share in Q3 or roughly 35% of its Free Cash Flow for the quarter.

Promising prospects and attractive valuation

The huge increase in CEIX’s stock price in 2022 was as a result of the expected improvement in earnings following the increase in the price of coal during the year. Markets are forward-looking but sometimes overshoot, so it’s important to question whether the stock price can continue rising. This requires investors to assess CEIX’s future prospects in relation to the current valuation.

CEIX’s prospects are, in my opinion, promising for two key reasons, which I will briefly outline.

The first is that the price of coal is likely to remain elevated in 2023 on record demand and continued tight supply. Despite its noble intentions, ESG investing has put a floor on prices of fossil fuels. Limiting new investments in any sector usually leads to supply scarcity and creates supernormal profits for existing sector players. This is what has happened with coal. Until the supply dynamic changes considerably, it is likely prices will remain elevated for a while.

The second reason is that CEIX will increase production significantly in 2023. It recently commissioned its Itmann mine in Wyoming, West Virginia. “For 2023, we expect higher sales volumes from both the PAMC and Itmann, which should add upside compared to this year,” said company CEO Jimmy Brock on the earnings call. Producing and selling more tons at an elevated price means better financial results.

It’s also worth noting that CEIX has reduced operating costs per ton sold by 24% from 2014–2021, according to its August 2022 investor presentation. Its projected growth for 2023 will therefore be value creating for shareholders thanks to improved margins.

When it comes to valuation, CEIX has a 5 year average P/E of 16.34 vs a current P/E (“FWD”) of 6.28x. Its current EV/EBITDA is just 3.21x. These multiples have room to grow in my opinion, and I wouldn’t be surprised if the stock continues its winning streak in 2023.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.