[ad_1]

ollo/iStock Unreleased via Getty Images

For a commercial property REIT, Global Net Lease (NYSE:GNL) has become somewhat of a controversial stock with bears flagging its externally managed structure as a core reason to avoid the commons. The bulls have raised the breadth of its diversity across geographies, industries, and property types as a reason to be bullish. The REIT focuses on sale-leaseback transactions involving single tenants in what it describes as ‘mission critical’ net-leased properties. This differs from triple-net lease properties in that Global Net Lease could also be responsible for a portion or all of the taxes, insurance, and maintenance costs for a property during the lease term.

What’s the controversy? The REIT is externally managed by New York-based AR Global, a $12 billion global real estate asset manager. External REITs can be a great way to gain exposure to certain property types if they have shareholder-friendly structures which prioritize FFO growth. AR Global is able to incur higher management fees on the basis that Global Net Lease’s asset base grows rather than FFO. Whilst this isn’t inherently bad if the REIT manager is able to acquire earning accretive properties at favourable cap rates, it could quickly form a conflict of interest. This would be in instances where the external manager starts to execute in a way that doesn’t fully optimize for shareholder value creation but for fee creation.

Growth At An Extremely Dilutive Cost

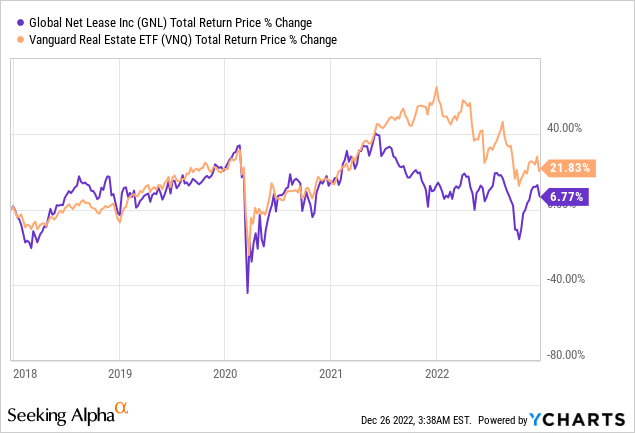

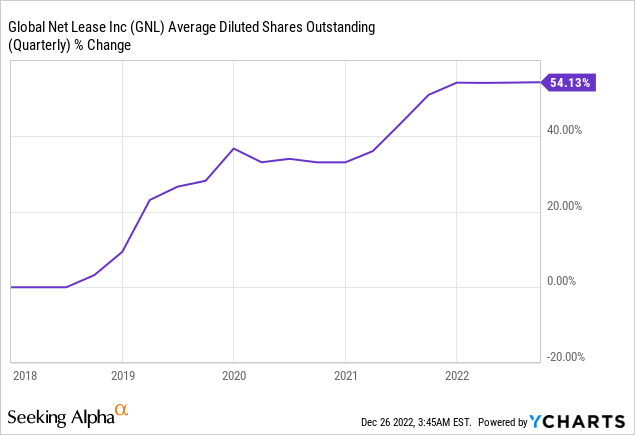

Global Net Lease’s five-year performance against a broad basket of real estate stocks like the Vanguard Real Estate ETF (VNQ) has been poor. The REIT is up 6.77% on a total return basis since 2018 versus total positive returns of 21.83% for VNQ. At the same time, Global Net Lease has increased its outstanding shares by 50%.

Issuing shares to fund new acquisitions again isn’t inherently bad and internally managed REITs occasionally do this. The difference is that it has come with significant underperformance for Global Net Lease. Under AR Global’s management, the commons have dropped by 61% but the manager has collected hundreds of millions of dollars in fees. Common shareholders are essentially paying to lose money. A fee structure that more easily rewards positive performance and FFO growth would, of course, be more beneficial and you can get that from any other comparable commercial property and internally managed REIT.

The Preferred Shares As An Option Against An Unfavourable Commons Structure

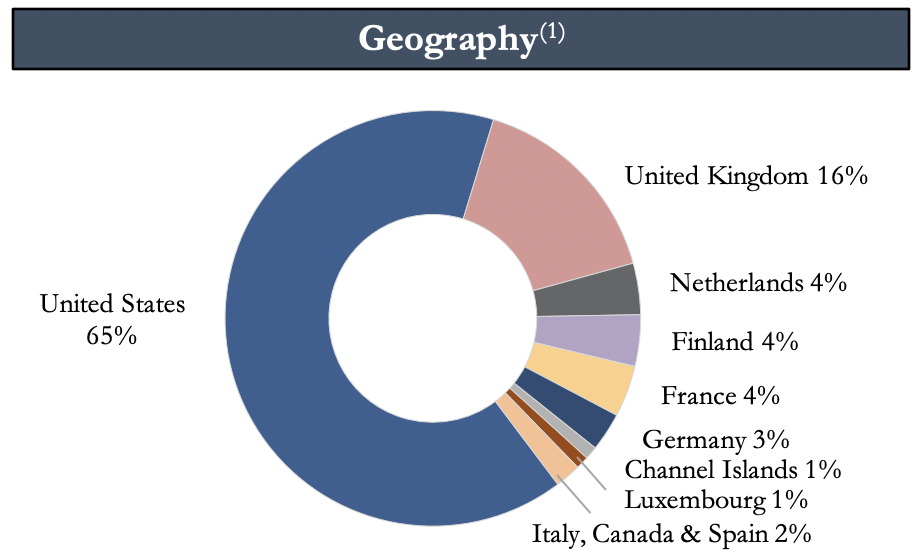

Global Net Lease last reported earnings for its fiscal 2022 third quarter. The company held 310 properties covering 39.5 million square feet across 11 countries and the Channel Islands as of the end of the quarter. The portfolio was 98.6% leased to 141 tenants, the largest of which is UK-based McLaren which accounts for around 6% of total straight-line rent.

Global Net Lease

Whilst such a relatively broad geographic spread exposes the REIT to foreign exchange risks, which would have been heightened this year due to the strong dollar, it reduces systematic risk from single-country exposure and would seemingly increase the overall safety of its commons.

Global Net Lease

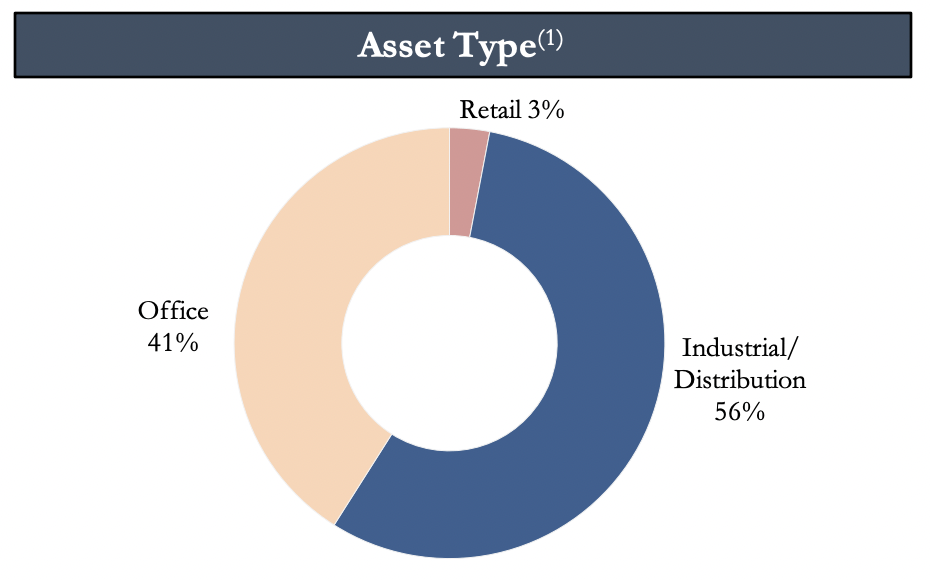

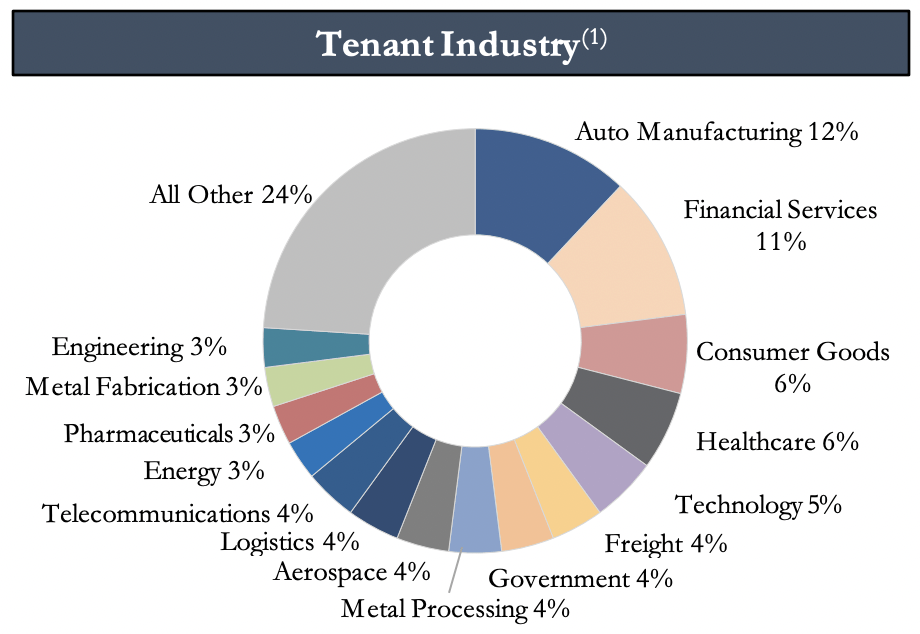

This inherent safety is compounded by the broadly diversified asset type. Global Net Lease is a hybrid office and industrial REIT with a marginal position in some retail properties at 3% of their portfolio. This is further diversified across a number of industries with financial services, auto manufacturing, and consumer goods forming the largest of these. 61.3% of its tenants are rated as investment grade, further increasing the safety of the company’s underlying portfolio.

Global Net Lease

Hence, the intention is clear. Global Net Lease has built diversification within diversification to reduce broader risk. It’s unfortunate then that its external management structure has built this back in. The diversified nature of its asset base brings its last quarterly per share cash dividend payout of $0.40 into view. Whilst the 12.4% yield would seem safe against a largely investment-grade rated tenant base spread across 11 geographies, it was actually cut at the onset of the pandemic from $0.53 per share. Its most closely comparable peer W. P. Carey (WPC) maintained its dividend payout and actually increased it toward the end of the same year.

The company’s adjusted FFO for its third quarter was $41.3 million, down 6.8% from $44.3 million in the year-ago comp. This meant that the REIT’s adjusted FFO per share was $0.40, down from $0.44 in the year-ago period. This barely covers the dividend payout and raises the spectre of a cut next year if macroeconomic conditions deteriorate to impact leasing demand and tenant bankruptcies.

Hence, the Series A Cumulative Redeemable Preferred Stock (NYSE:GNL.PA) offer an alternative method of exposure. They have a hard per share intrinsic value of $25 which Global Net Lease can pay at any time as they are trading past their September 12, 2022 call date.

QuantumOnline

They also pay out a $1.81 coupon in quarterly instalments for a yield of 8.5% against their current price. The bond-like $25 redemption value of the preferred shares is a core mechanic that makes them attractive. Holders will be eligible for a cash payment of $3.76 per share in the event of a redemption, which would be a return on top of the annual coupon. They also rank higher on the capital structure than the commons, hence, the coupon is unlikely to be affected in the event Global Net Lease is forced to pare back in common share dividend payout.

However, it’s important to note that these are down 19.73% year-to-date, a worse performance than the commons and could fall further to a discount to their NAV if holders of the preferred shares sell out on perceived risk. I’m not a buyer here but can see the appeal.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.