[ad_1]

courtneyk

Since my last article covering the SPDR S&P Regional Banking ETF (NYSEARCA:KRE) (August 2021), regional banking stocks have performed relatively well; according to Seeking Alpha, KRE’s total return (since August 23, 2021) was 0.64% against the S&P 500 index’s price-only change of -7.19% (KRE’s price change: -1.56%). Absolute returns have been negative for most equity ETFs due to general risk aversion, recessionary fears (apparently largely due to inflationary pressures), and other ancillary risks (such as war between Russia and Ukraine).

The SPDR S&P Regional Banking ETF is an exchange-traded fund that enables investors to get financial exposure to the S&P Regional Banks Select Industry Index; this index is KRE’s benchmark, that it seeks to replicate. The fund is wholly exposed to the United States, geographically; for the uninitiated, “regional” is a reference to banks (depository institutions) that typically offer conventional banking and savings and loan offerings at a state level (larger than a community bank; but smaller than a national bank).

The banking sector is, of course, long-established, largely mature (leaving aside emerging financial technologies; the banks of course have to continue to invest in order to compete with other banks), and generate stable returns on equity. Due to variable interest rates on loan products, and low interest rates offered on deposits, banks are sometimes viewed as less risky in inflationary regimes. They are not quite a “hedge against inflation”, although some investors may increase exposure to banks during rising interest rate regimes (such as right now) even in spite of elevated inflationary pressures.

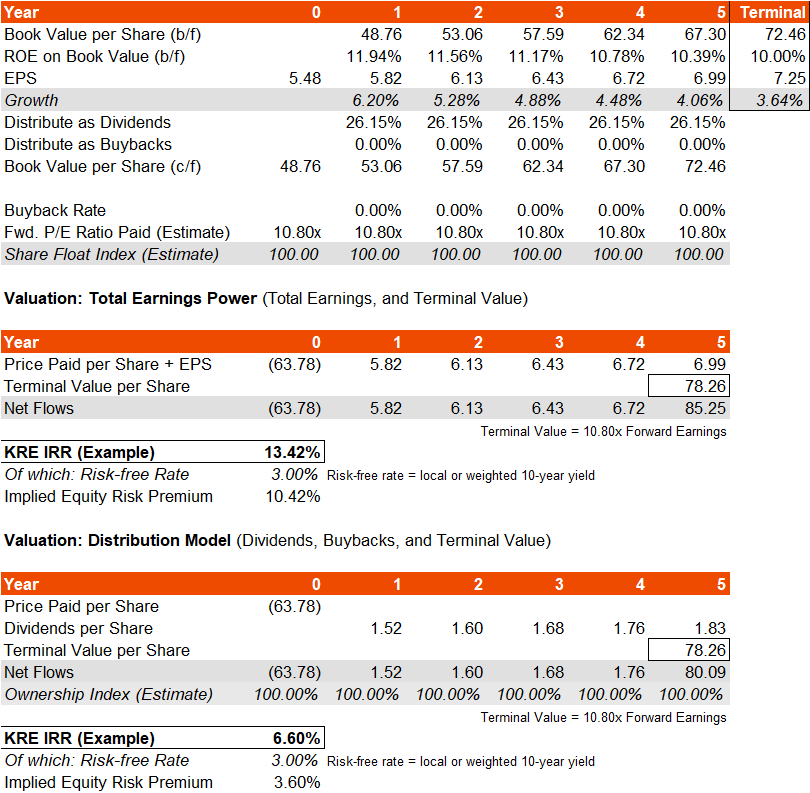

KRE had assets under management of $3.06 billion as of July 28, 2022, with a gross expense ratio of 0.35%. Based on data provided by SPDR themselves, the projected 3-5 year average earnings growth rate was 8.50% as of July 28, 2022, with 144 holdings, a price/book ratio of 1.29x, and a forward price/earnings ratio of 10.80x. The 30-day SEC yield (an approximate dividend yield) was 2.28%. Based on this data, we can impute a forward return on equity of circa 12%, and a distribution rate (without buybacks) of 26%.

If we assume that the return on equity drops off to about 10% over several years, we come to a three- to five-year earnings growth rate of 4.98-5.45%, which is a lower range than our projected figure above (provided by SPDR, from consensus analyst estimates) of 8.50%. My lower figure also compares to Morningstar‘s even more optimistic figure of 9.10% over the same time frame. In any event, based on this possibly conservative assumption of mine, and assuming no buybacks, I arrive at a forward IRR of circa 6.60-13.42%.

Author’s Calculations

If we assume no buybacks for simplicity and only value the dividend yield, the implied equity risk premium is 3.60-4.00% (I assumed a risk-free rate of 3%, although this is higher than the U.S. 10-year yield which is currently under 2.70% at the time of writing). If we value KRE on total underlying earnings power, the fund seems to offer better value, with an ERP of over 10%. Bear in mind this fund has historically generated a higher beta than broader equity indices though, of circa 1.27x, so you could arguably scale back my ERP estimate of 10.42% (above) to 8.20% on an adjusted basis. This is still high; for mature markets, we would expect something between 3.20-5.50%.

So, in theory, KRE is undervalued still, and this possibly does make sense. I believed KRE was undervalued all considered back in August 2021; while it has out-performed broader equity indices, those indices have fallen, and so absolute returns have still been negative. An expansion of equity risk premia across the broader equity market has led to falling valuations, and that has led KRE to suffer all the same (only apparently to a lesser extent).

Also, if we assume that KRE deserves a long-term equity risk premium of 5.50%, a risk-free rate (for our analysis) of 3%, and a long-term earnings growth assumption of about 2% (nominal), we would arrive at a growth-adjusted cost of equity of 6.50% (that is, 5.50% + 3.00% – 2.00%). Dividing forward earnings into this figure gives us an immediate capitalization value of about $89.54 per share. That is almost exactly 40% above the current share price of KRE.

Even if we head into a recession, and the increasingly “data dependent” Federal Reserve pivots on its monetary policy and even looks to ease rates over the next one or two years, KRE is likely to offer decent value. Under-cutting consensus analyst estimates has still led me to believe that plenty of upside is available in KRE on valuation alone.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.