[ad_1]

Andy Feng

China is now taking steps to move away from zero-Covid policies, but the process will clearly be painful for Chinese stocks in the months ahead. NIO (NYSE:NIO) is a potential global force in the EV market, but years of Covid restrictions have impacted near-term production numbers. My investment thesis is Bullish on Chinese stocks, with business poised to rebound in 2023.

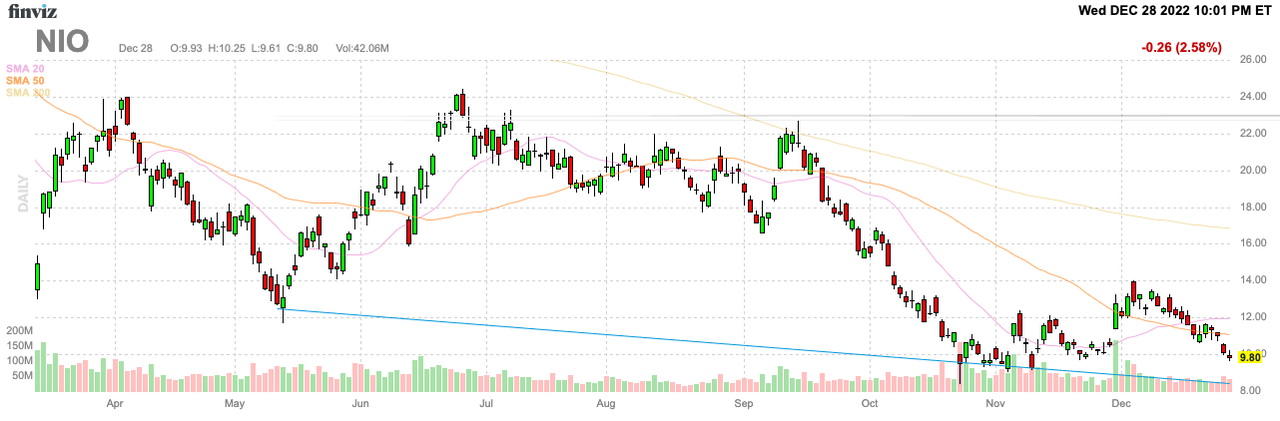

Source: FinViz

Q4 Delivery Hit By Covid

As the holiday quarter comes to an end, NIO reported deliveries failed to come close to expectations. The stock fell 8% on the news, but the damage was done in previous periods, with NIO not even printing a new 52-week low on the negative news.

The NIO CEO warned of a tough 1H of 2023 due to the supply chain issues. The reason to turn bullish on NIO and the Chinese sector is the sudden flip on the zero-Covid policy.

China announced a plan to further open the economy on Wednesday, with unrestricted international travel. The market got spooked by the US announcement of the requirement for a negative test to enter the country from China.

Considering Covid is spreading fast in China and sick passengers were loaded on flights to Milan, the US move is probably prudent over a short period to keep the infected from traveling. Though, the policies clearly aren’t going to revert to prior lockdowns after the US has been fully reopened.

The communist country is already estimated to have seen up to 250 million Chinese infected by the virus through December 20 with some 37 million people being infected on a daily basis. At this rate, half the country will have been infected by early January and natural immunity will start taking hold.

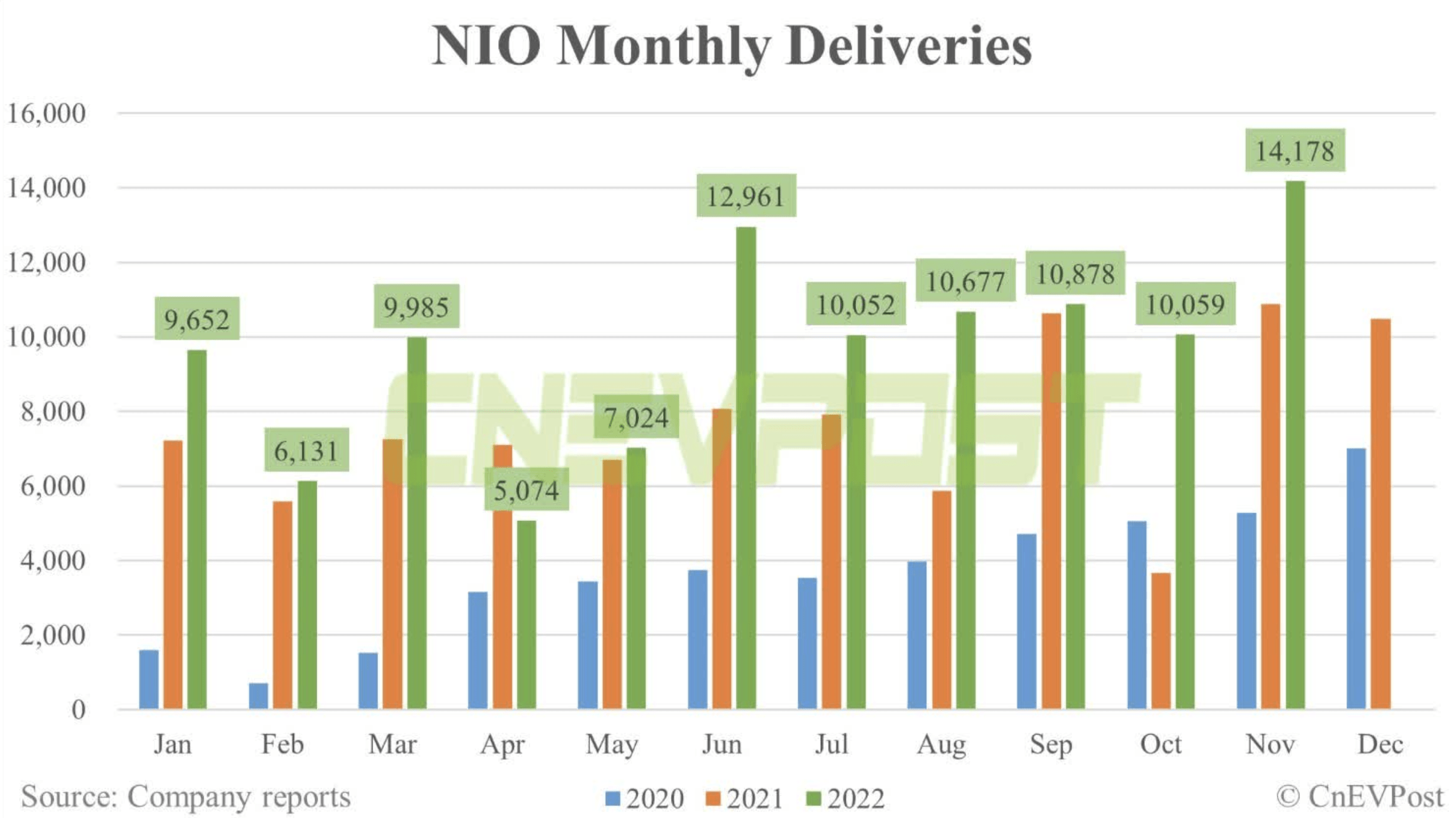

The pace of the Covid infections is encouraging that the impact within China will be short-felt. NIO guided to Q4 deliveries of 38,500 to 39,500, down from a prior estimate of 43,000 to 48,000. The company targets ~14,763 deliveries in December for a new record high, slightly up from the November total of 14,178.

Source: CnEVPost

The updated guidance actually maintains solid growth YoY as NIO was still working to rebound from Covid restrictions in prior periods. The EV company should produce ~121,500 EVs this year, setting up an easy hurdle for 2023 with or without headwinds.

NIO is working on an annualized production rate of 177,000 units for 2023. Even just extrapolating the Q4 production rate gets the company to nearly 160,000 units for the year, vastly above the 2022 production despite the disappointing end to the year.

The company made the following statement along with the CEO highlighting consumer confidence and supply chain issues restricting vehicle production:

While our teams have strived to maintain continuous operations on all fronts, we were not able to reach our full capacities, particularly when there have been disruptions on delivery and registration procedures involving users

Better 2023

All of these headwinds add up to a better 2023. Investors need to watch out for a tough January delivery metric, with the whole country of China possibly infected by unleashing Covid starting in December. As the skies clear in early 2023 after people take a week or two to recover from Covid, confidence in the economy should return.

At NIO Day 2022 in Hefei, China, the company launched the EC7 and the All-New ES8. These new SUVs will commence delivery in May and June 2023, respectively.

NIO continues to aggressively move forward with battery-swapping technology and autonomous vehicle advancements. The investment story hasn’t changed, but the Covid story has been volatile and is now becoming a tailwind to start the new year.

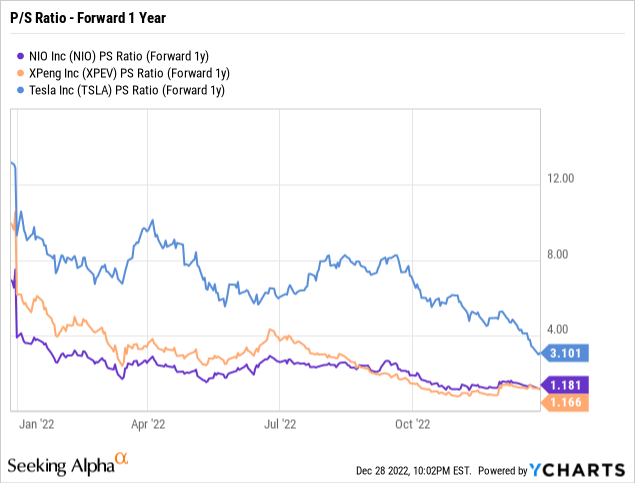

Similar to XPeng (XPEV), NIO now trades at only 1.2x forward sales targets. The stocks continue to trade at a fraction of the valuation of Tesla (TSLA), which currently trades at 3.1x forward sales.

Analysts forecast sales jumping to $14 billion in 2023 followed by a 32% jump to $18 billion in 2024. After a speed bump to start 2023, investors should have confidence the inevitable full reopening gets the Chinese economy back into growth mode, which could push NIO to the next level.

The stock once traded above $60 when NIO wasn’t even producing $1 billion in quarterly sales. The stock probably won’t hit the premium P/S multiples of prior periods, but an investor only needs a 2x to 3x forward P/S multiple to generate superior returns.

Takeaway

The key investor takeaway is that NIO is a good investment at these levels to ride the rebound in the Chinese market. The company should report strong growth in 2023 and the combination with the reopening of the Chinese economy should send investors flooding into the stock when better times return next year.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.