[ad_1]

Uwe Krejci

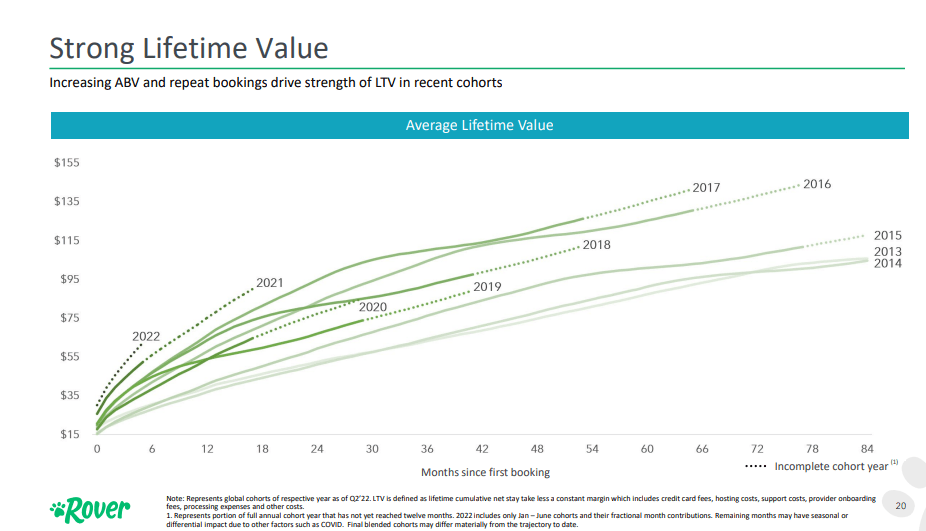

Rover (NASDAQ:ROVR) reported another strong quarter, even if guidance for next quarter was a little bit below expectations. In addition to solid numbers for the reported quarter, there were also some positive news on other fronts. For example, the company shared that the lifetime value of customers acquired this year is the highest to date. Revenue per customer, less the cost of revenue and support, are trending higher than the 2021 cohort, which was already one of the best cohorts.

Rover Investor Presentation

This leads us to continue believing that this is a high growth company with attractive customer unit economics, and therefore a lot of potential. One disappointing thing was that cancellation rates saw an uptick towards the end of the quarter, and that is one of the reasons why they are reducing guidance for next quarter. While the company delivered a strong second quarter and continued to gain market share, the company sees reasons to be cautious for the second half of the year. The company is therefore slowing down hiring and marketing spend.

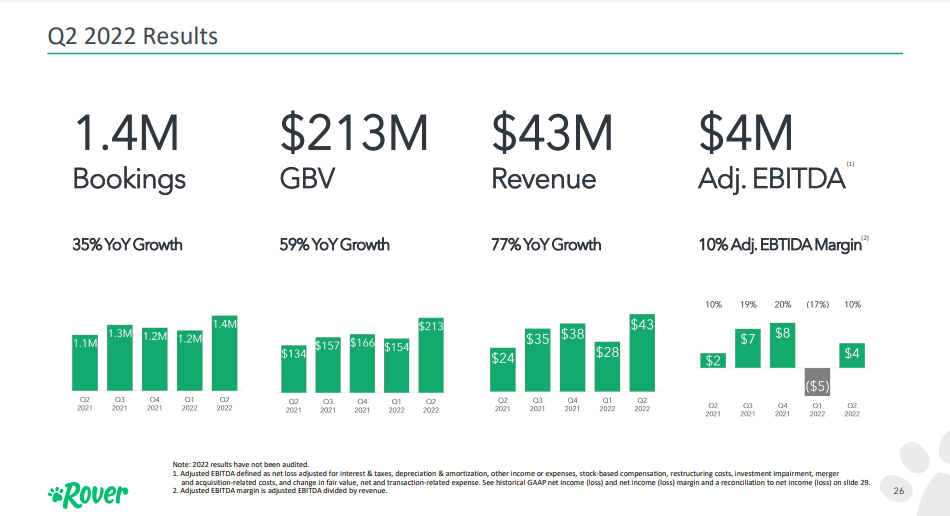

Q2 2022 Results

The main stats for Q2 2022 results are shown below, note that GBV continues to grow nicely, thanks to a combination of growth in bookings and spend per booking. The largest absolute growth in international markets came from Canada and the UK. The company was profitable again on an adjusted EBITDA basis, with a ~10% adjusted EBITDA margin. Revenue increased even faster than GBV as the company’s take rate increased.

Rover Investor Presentation

Financials

Second quarter revenue exceeded guidance, thanks to increases in average booking value and strength in European bookings. Meanwhile, second quarter average booking value was $147, up 18% y/y, driven by increases in average service price by pet care providers. This growth in ABVs, along with solid retention rates, has increased expected LTVs.

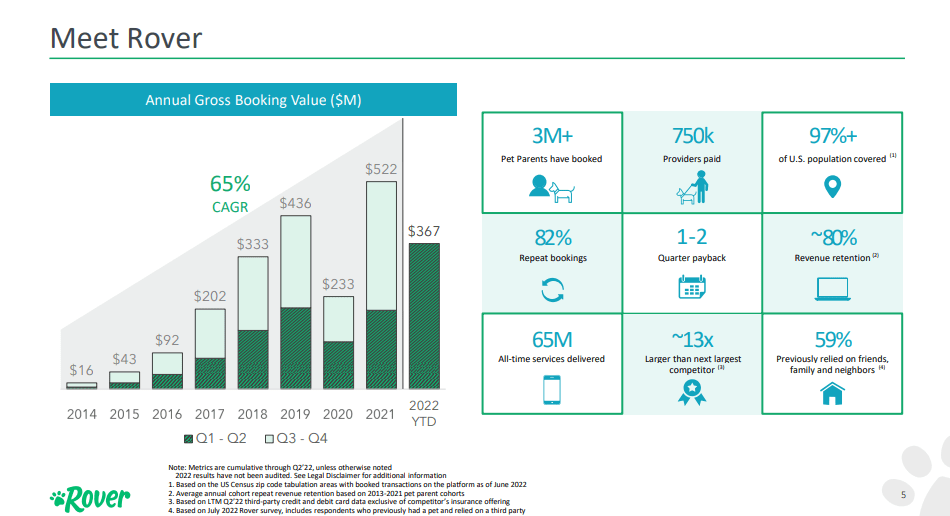

For us the most important KPI remains annual gross booking value, which is quickly approaching $1 billion.

Rover Investor Presentation

Valuation

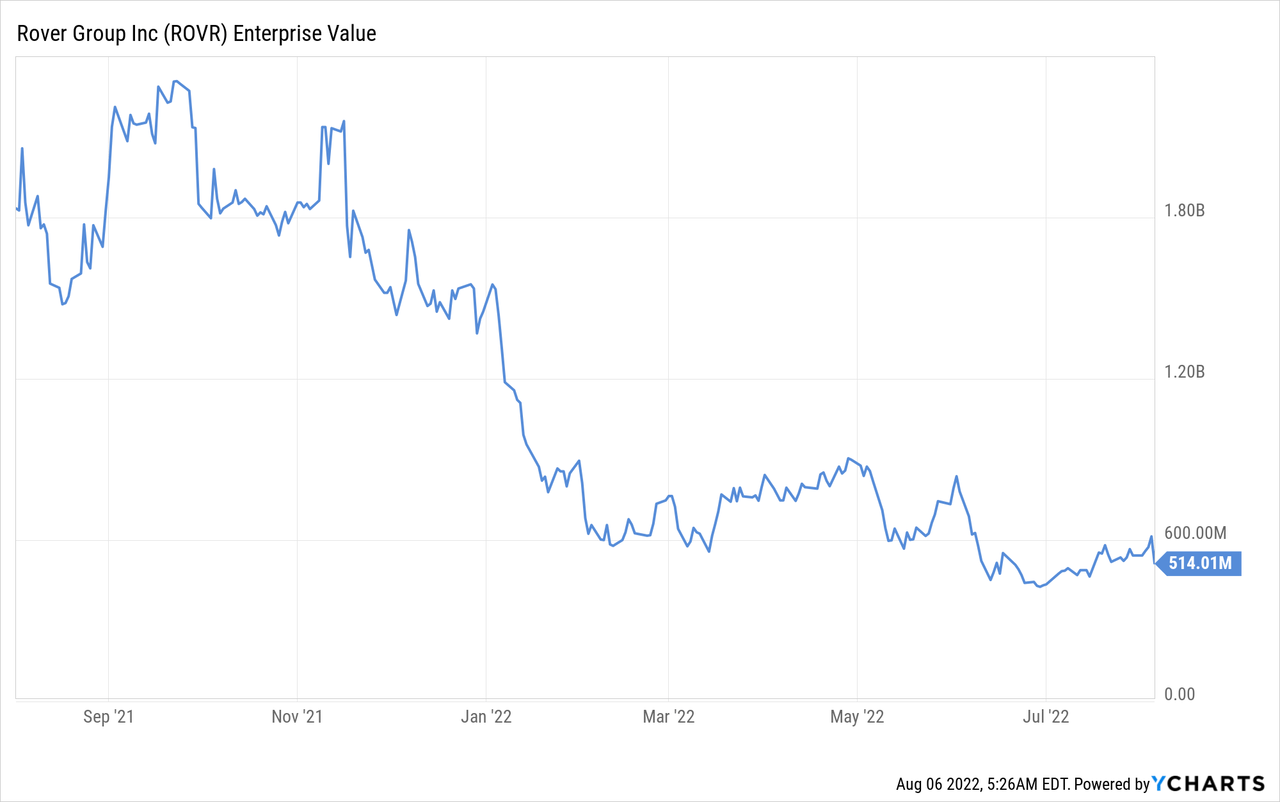

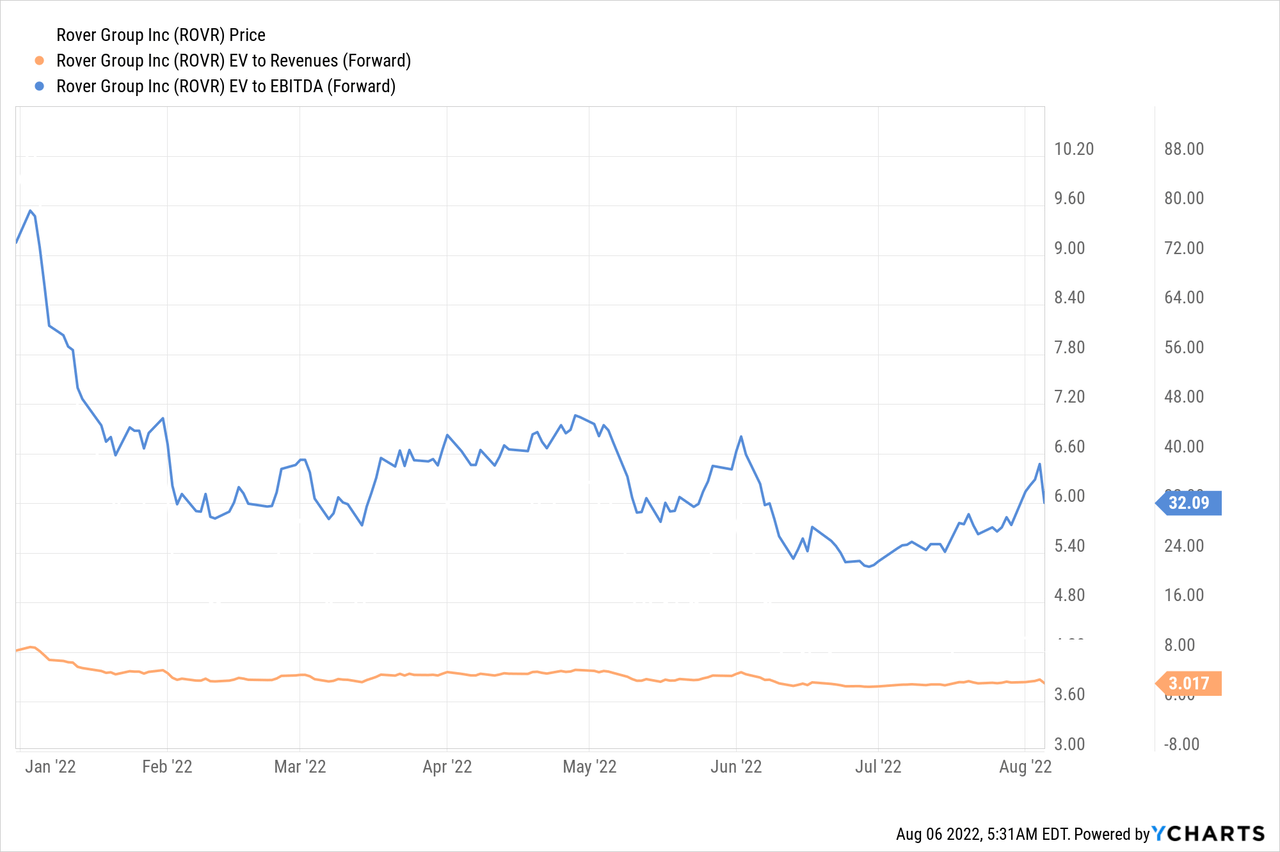

The company continues to hold a large amount of cash, equivalents, and short-term investments. That is why the enterprise value is significantly below the market cap. The enterprise value is currently about $500 million, which is below the expected annual gross booking value, which is one reasons we believe the company is undervalued.

For a platform company with network effects and strong competitive advantages, and very high gross margins, we believe that shares are currently valued too low at ~3x forward EV/Revenues. While at this stage we would not put too much weight on EBITDA estimates, shares also look cheap with a forward EV/EBITDA of ~32x, especially given that revenues and earnings are expected to continue growing at a very fast pace for several more years.

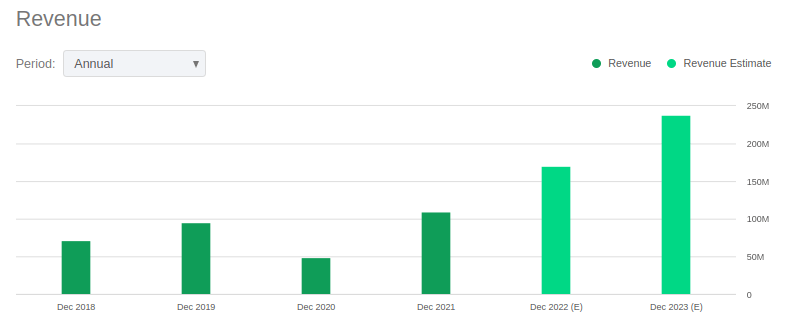

For 2023 analysts are expecting revenue to reach almost $250 million, which puts the EV/Revenues based on FY23 estimates at only ~2x.

Seeking Alpha

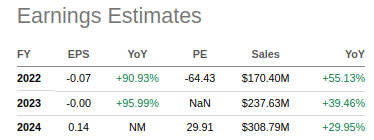

Looking at EPS estimates, as compiled by Seeking Alpha, estimates are for a $0.14 profit per share for 2024, which would place the price/earnings ratio at ~29.9x. This might not seem like a bargain, but for a company that is growing revenues at 77% y/y, and that has a lot of room to expand EBITDA margins, we believe it is cheap.

Seeking Alpha

Guidance

The company updated the guidance for Q3 2022 and full-year 2022. For Q3 2022 revenue is expected to be in the range of $46 – $48 million, and Rover anticipates Adjusted EBITDA in the range of $6 – $8 million. For the full-year 2022 Rover anticipates revenue in the range of $160 – $166 million, a year-over-year increase of 48% at the midpoint of the projected range, and Adjusted EBITDA in the range of $10 – $14 million.

Both the low and high end of revenue guidance continues to assume the full year impact related to Omicron and the recent macroeconomic headwinds, inclusive of elevated cancellation rates and softer new customer demand, as aligned with the macro slow-downs seen in TSA growth and Google query volume. The high end of guidance differs from the low end by assuming more modest impacts of additional Covid waves, and no further incremental deterioration in demand due to macroeconomic trends.

During the earnings call, management reiterated their longer-term margin goal of over 30% for the core business.

Conclusion

We continue to believe Rover is an attractive platform business growing at a rapid pace, and with improving financials. Shares look attractive on a number of valuation measures, including forward EV/Revenues, and EV to annual gross booking value. We believe the company has competitive advantages, including networks effects from the two-sided marketplace it operates, and from the data and proprietary algorithms it is continuously improving to make better matches. Despite some disappointment in the reduced guidance for Q3, and for the rest of the year, we still see a lot to like about the company.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.