[ad_1]

Torsten Asmus/iStock via Getty Images

Sitio Royalties (NYSE:STR) completed its merger with Brigham Minerals near the end of 2022. This has resulted in a Permian-focused mineral and royalty company with approximately 33,500 BOEPD (50% oil) in production.

As a mineral and royalty company, Sitio is insulated from the direct impact of the cost inflation issues that are affecting many producers. However, it is still affected by lower commodity prices and is mostly unhedged for 2023. At current strip (including $74 WTI oil) for 2023, I estimate that it will generate $2.65 per share in distributable cash flow now.

Sitio’s distributable cash flow is also impacted by its high interest 2026 notes, which have a variable interest rate tied to SOFR. These notes now have an interest rate that is over 10%.

Despite that, I believe that Sitio is somewhat more attractive now at a bit over $25 per share compared to when I looked at it in October, since its share price has gone down around 9% since then.

I believe that Sitio is now fairly priced at around $27 per share for a long-term $70 WTI oil and a $4 NYMEX gas environment.

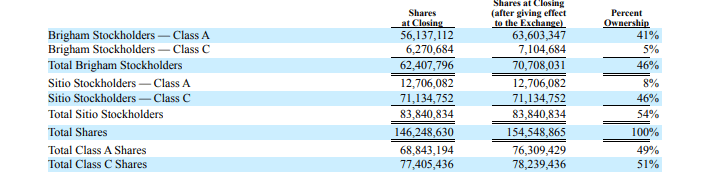

Share Count

The filings indicate that there were 62.4 million Brigham shares at closing, which were exchanged into 70.7 million Sitio shares based on the 1.133 Sitio shares to 1.0 Brigham share exchange rate.

There were 83.8 million Sitio shares at closing, and after the exchange there were 154.5 million Sitio shares outstanding.

Sitio’s Share Count (sitio.com (Proxy Statement))

Legacy Sitio shareholders end up with 54% of the post-closing shares, while Brigham shareholders end up with 46% ownership.

Cash Balance

The combined company had $50 million in cash (including restricted cash) and $740 million in debt at the end of Q3 2022. However, Brigham’s $132.5 million cash acquisition of mineral and royalty interests from Avant Natural Resources hadn’t yet closed by the end of Q3 2022. Pro forma for that acquisition, the combined company’s net debt would be approximately $820 million.

Sitio’s Balance Sheet (sitio.com (Proxy Statement))

This may be reduced to approximately $780 million in net debt by the end of 2022.

2023 Results Based On Current Strip

Sitio bumped up its expected (combined company) production for the 12 months ending June 2023 to approximately 33,500 BOEPD (50% oil). This is also around its Q3 2022 production. I am thus going to continue to model Sitio’s full-year production at around 33,500 BOEPD (50% oil).

The current strip for 2023 is now around $74 WTI oil and $3.70 NYMEX gas. At those commodity prices, Sitio may be able to generate $601 million in revenues, including hedges. Sitio’s 2023 hedges have an estimated value of positive $25 million at those commodity prices.

|

Type |

Barrels/Mcf |

Realized $ Per Barrel/Mcf |

Revenue ($ Million) |

|

Oil (Barrels) |

6,113,750 |

$73.50 |

$449 |

|

NGLs (Barrels) |

2,445,500 |

$25.50 |

$62 |

|

Natural Gas [MCF] |

22,009,500 |

$2.70 |

$59 |

|

Lease Bonus and Other Revenues |

$6 |

||

|

Hedge Value |

$25 |

||

|

Total |

$601 |

Sitio has $450 million in unsecured senior notes due 2026 with a variable interest rate that appears to be pretty high. Now that the Brigham merger has closed, these notes bear interest based on the adjusted Term SOFR rate + 5.75%. The three-month Term SOFR rate is currently around 4.6%, so the interest rate on the notes is over 10%.

Interest On 2026 Notes (sitio.com (Q3 2022 10-Q))

Sitio is now projected to have $191 million in cash expenditures in 2023, leaving it with $410 million ($2.65 per share) in discretionary cash flow.

|

$ Million |

|

|

Production Taxes |

$40 |

|

Gathering And Transportation |

$18 |

|

Cash G&A |

$22 |

|

Cash Interest |

$60 |

|

Cash Taxes |

$51 |

|

Total Expenses |

$191 |

At a 65% payout ratio, this would result in $1.72 per share in dividends related to 2023 results and $144 million for debt reduction. This would leave Sitio with $636 million in net debt at the end of 2023, or leverage of 1.2x.

Estimated Valuation

I am now estimating Sitio’s value at around $27 per share in a long-term $70 WTI oil and $4.00 NYMEX gas environment. Sitio’s value has been reduced a bit by the high interest costs on its 2026 notes, which cut into its distributable cash flow. Sitio may pay around $0.39 per share in interest costs in 2023, most of which are related to its 2026 notes. Sitio can reduce its interest costs over time with debt paydown, although this would require it to maintain a payout ratio well below 100% as it does so.

Conclusion

Sitio Royalties recently completed its merger with Brigham Minerals. It expects to produce approximately 33,500 BOEPD (50% oil) over the next little while, which is a level that would result in around $2.65 per share in distributable cash flow in 2023 at current strip prices ($74 WTI oil).

Sitio’s interest costs are a bit higher than ideal due to the 10+% current interest rate on its variable interest rate 2026 notes. That being said, Sitio appears to have a modest amount of upside (to $27 per share) in a long-term $70 WTI oil environment, while also potentially offering a near 7% yield at a 65% payout ratio.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.