[ad_1]

Torsten Asmus

As many investors are aware, the economy has officially entered a recession with two negative quarters of GDP growth. There is general fear that commodities will drop in 2022 like they dropped in 2008. In this article, I will debunk this myth in 5 simple charts. I believe we are currently in an entirely different environment compared to 2008 and this time will be different.

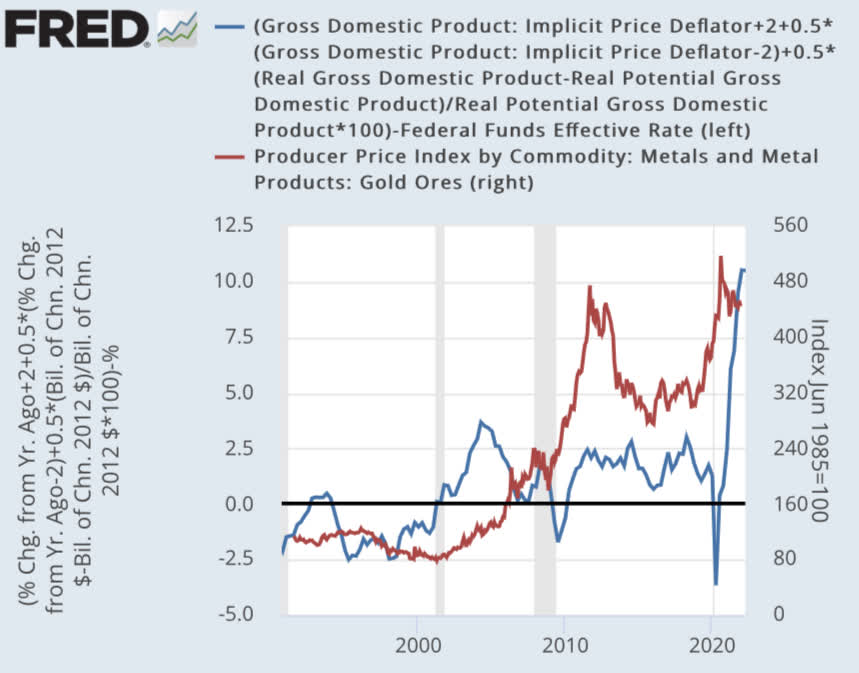

The first chart shows the Taylor Rule Rate minus the Fed Funds Rate. Whenever this chart is above zero, this means that the Federal Reserve’s effective Fed Funds rate isn’t high enough to tame inflation. That number is currently above 10% and has historically never been this high. Since the Federal Reserve isn’t going to hike rates to 10%, I expect that inflation will continue to persist well into the future and support commodity prices.

FRED

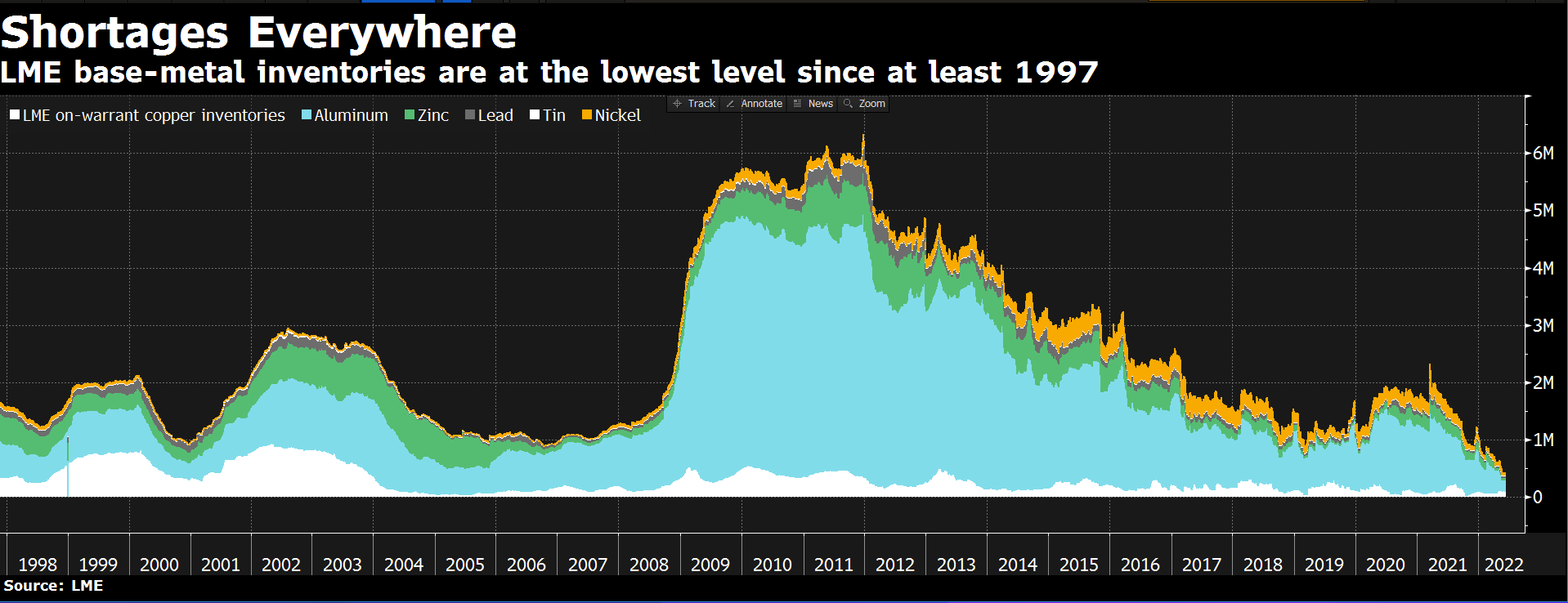

Second, LME inventories are currently at an extremely low level. Whenever levels get this low, prices tend to rise due to shortages. In 2008, commodities were in a period of glut when inventories rose. Today, we are in a period of shortage where inventories are falling. The base metal inventories in the chart below have fallen to a record low, with aluminum at an extreme level. Oil and gas inventories are equally at very low levels today. Moreover, the U.S. strategic petroleum reserves are currently being depleted as we speak.

LME

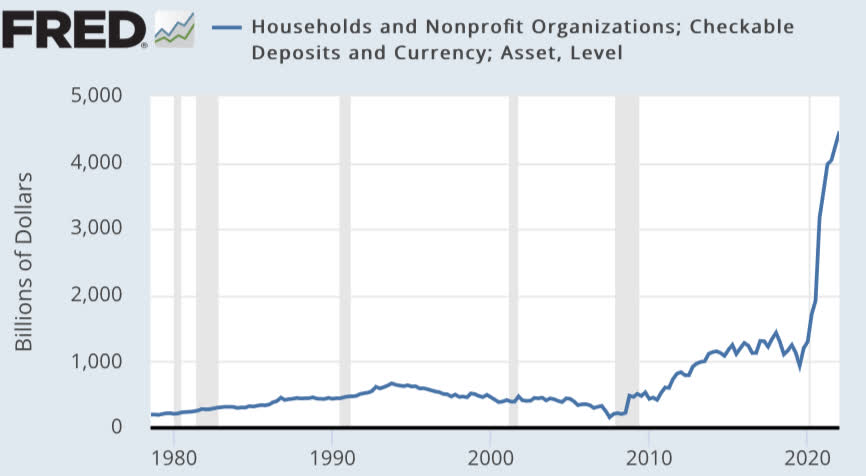

Third, as inventories are dwelling, the consumer is having plenty of savings to buy stuff. Household and nonprofit organizations held the most deposits in history due to the massive money printing from the Federal Reserve. In contrast, 2008 saw a depletion of deposits. So we certainly don’t have a liquidity crisis today.

FRED

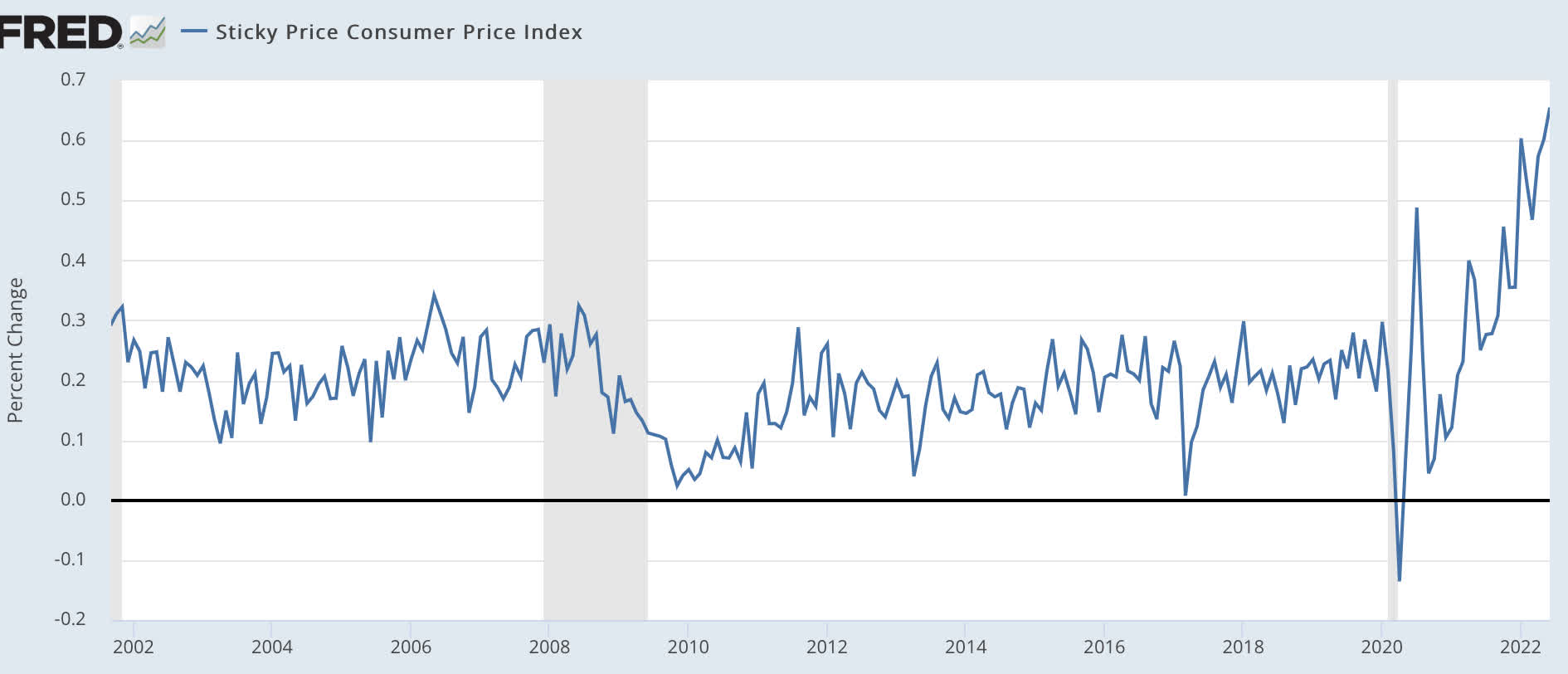

Fourth, due to consumers having plenty of savings, this has resulted in sticky inflation. As wages started to rise, inflation has now been embedded in consumer prices. So not only do we have less supply, we are also seeing increasing pressures on the demand side, which is going through the roof.

FRED

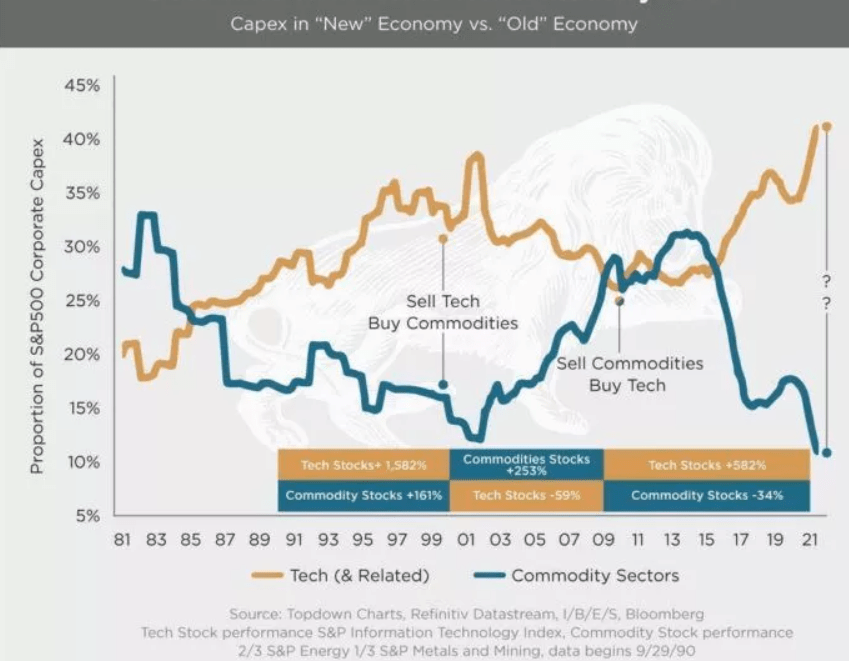

Finally, Topdown Charts reports that we are currently in a low CAPEX cycle for commodities while in a high CAPEX cycle for technology. Whenever CAPEX is low, this typically marks a bottom in the underlying sector. As prices rise, CAPEX will rise with it as it incentivizes more investment into that sector. 2008 was a period where CAPEX was high for commodities. Today we are at the complete opposite situation where we are not seeing any investment in commodities. For example, oil companies are not investing in drilling activities or refineries. They are just paying out dividends to investors.

Bloomberg

In conclusion, 2022 is very different from 2008 in light of the factors I discussed above, and we shouldn’t assume that a recession will lead to a drop in commodity pricing. I believe commodities are still in a long-term bull market and advise investors to take a position in size.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.