[ad_1]

JHVEPhoto

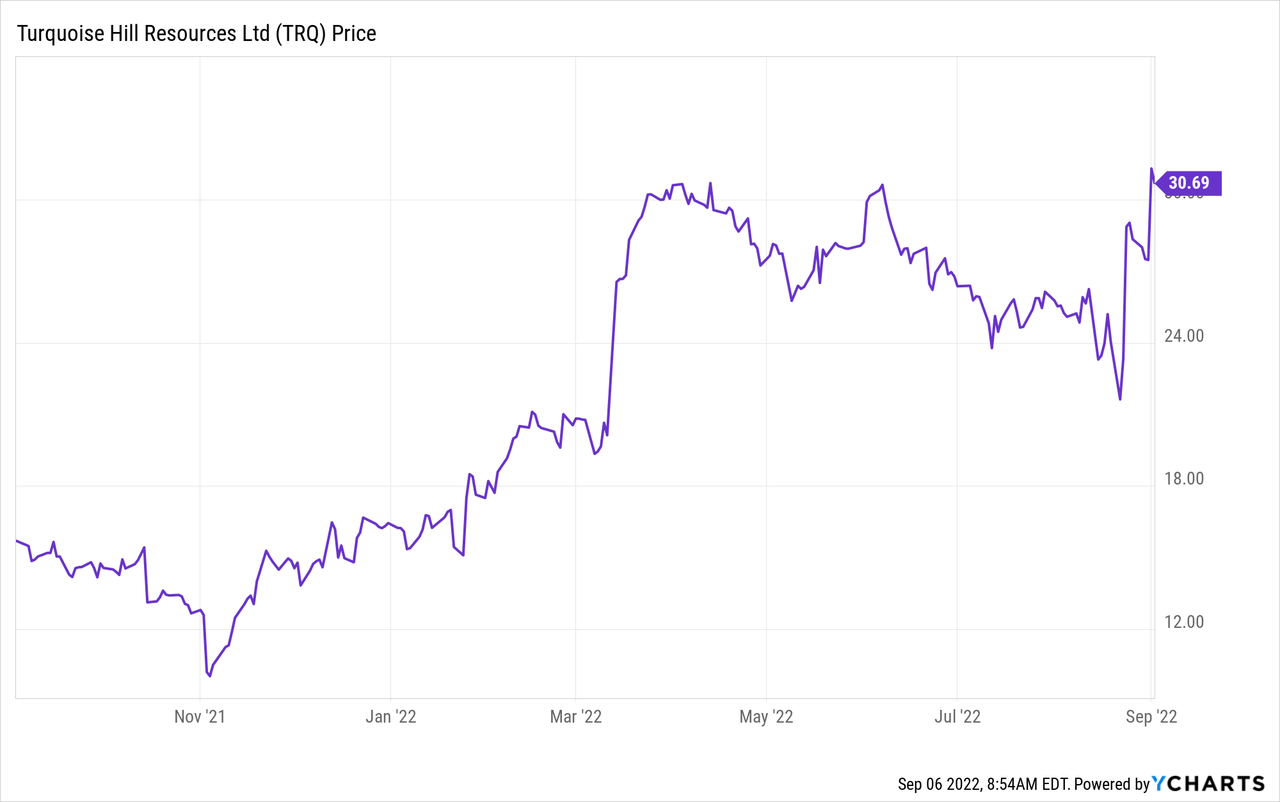

Turquoise Hill Resources Ltd. (NYSE:TRQ) has signed a definitive merger agreement with Rio Tinto Group (RTPPF, RTNTF, RIO,). Rio is buying out the remaining minority shareholders (except the Mongolian government, which will hang on to a 34% stake) at C$43 per share.

Pre-market, the stock is trading at $40.36. If I buy at the premarket price, I’d see a ~$6.5% gain as my stock is taken out. That’s quite attractive because Rio Tinto has worked with Turquoise Hill for many years and maintained an equity stake. It is going into this deal with tremendous knowledge about the situation it is getting into. Rio isn’t acquiring a large business at a huge business, but it is picking up an additional ~15% of shares outstanding. In my experience, this makes it a deal that’s much less likely to get derailed and much more likely to close as planned and quite quickly.

TRQ expects to hold a special shareholder meeting in the fourth quarter of 2022. If approved (66% threshold of minority shareholders), the deal should close shortly afterward.

The downside, if the deal fails, could be pronounced, though. In addition to a nice premium, the deal also encompasses Rio providing TRQ with some financing (a not insignificant $1.1 billion) to assuage short-term liquidity needs.

This $1.1 billion would have to be refinanced through an equity raise in the first six months of 2023. The deal failing will take some time; after it does, TRQ would immediately be faced with a bad situation. Deals tend to fail at times when capital markets are stressed and liquidity “less plentiful,” so I can imagine painful scenarios.

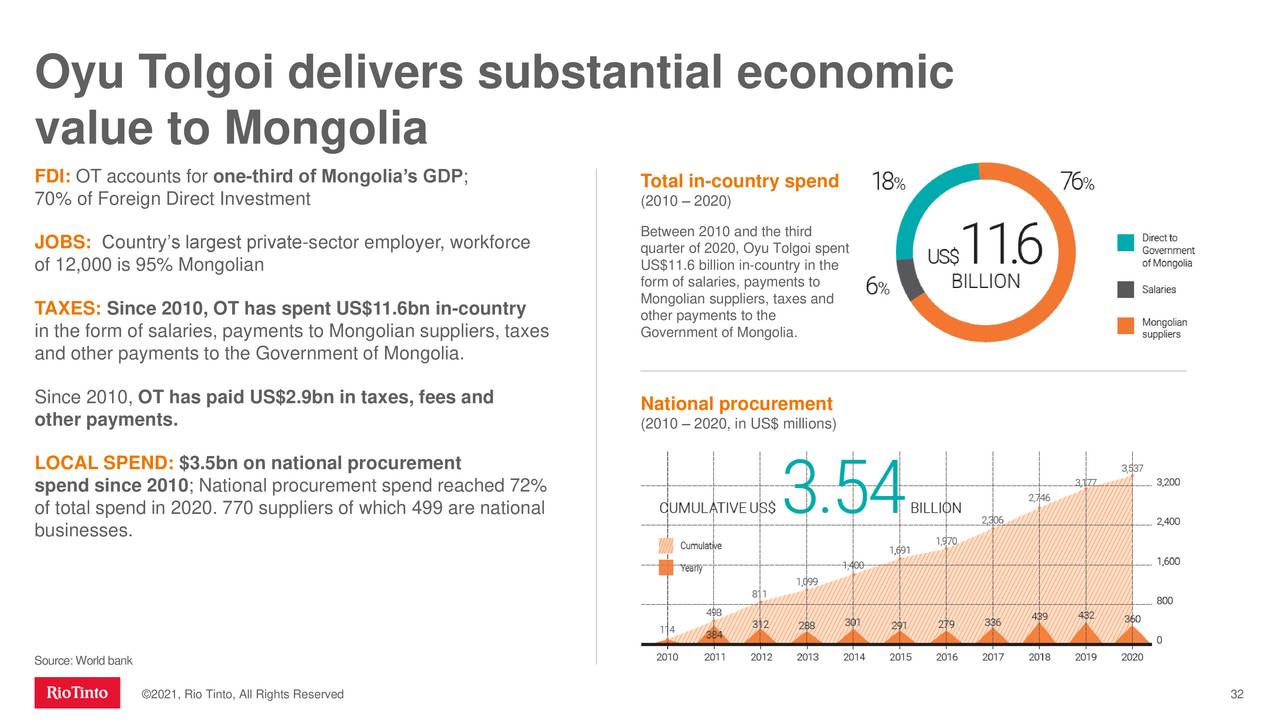

I believe this transaction is also good news for Mongolia. Sustainable production at the mine is expected to be ongoing H1’23. It may sound incredible, but I flagged the mine as a potential strong tailwind for a tiny Mongolian company in an unrelated business I looked into. Here’s an excerpt of what I wrote at the time:

Mongolia has an estimated GDP of slightly below $14 billion. The Oyu Tolgoi mine alone employs 12.000 people (95% Mongolian). According to the World Bank, this project alone may account for 30%+ of GDP.

The World Bank calls Mongolia a vibrant democracy that has tripled its GDP per capita since 1991. Primary school enrollments are at 97%. There has been an impressive decline in maternal and child mortality over the past decades. It also calls Mongolia’s development prospects “promising in the long-term assuming the continuation of structural reforms.” Here’s the most recent economic update.

Rio Tinto also published a slide showing the benefits of the mine to the Mongolian economy:

Oyu Tolgoi Mine vaue to Mongolia (Rio Tinto)

Because of several secular growth drivers like the energy transition(electrification, renewables, energy storage) and India’s economic growth, combined with a supply picture that doesn’t seem to evolve at a similar breakneck speed, I’m quite bullish on copper over a longer time frame. The current trajectory of the Fed isn’t outright bullish, of course. I’m in the camp that believes Powell may continue to tighten as conditions deteriorate (all bets are off if the real economy weakens significantly). This is a roundabout way of saying, no matter the copper price or outlook in the short term, there’s a good chance Rio Tinto wants to close this given the long-term prospects of copper.

The odds of picking up 6.5% in a quarter seem high. It is a large pre-market spread on a deal with such a high level of certainty.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.