[ad_1]

guvendemir

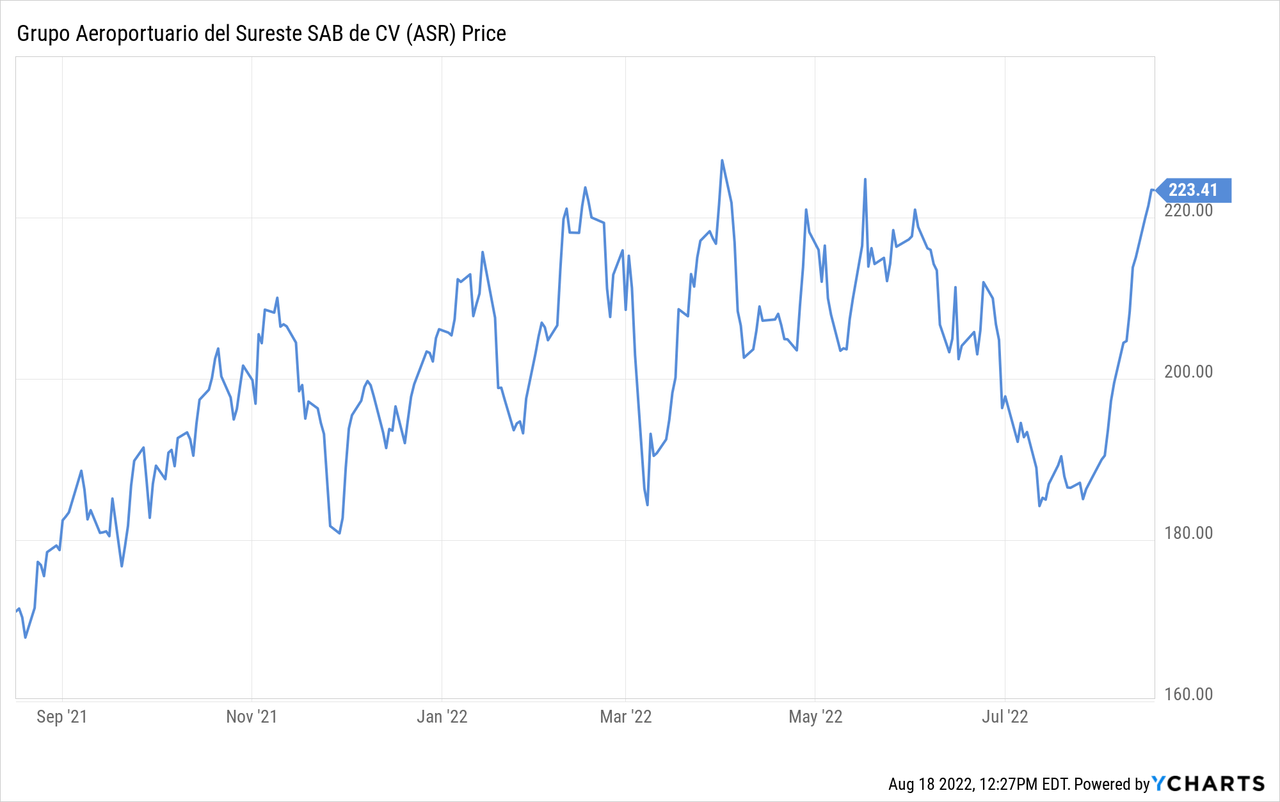

Some might feel that with prices close to the 52 week high, it is too late to buy shares in Grupo Aeroportuario del Sureste, or ASUR (NYSE:ASR), the Cancun airport operator. When looking at the valuation, and the Q2 2022 results, however, we believe there is still more upside to be had for investors with a long-term horizon. The valuation is definitely still cheap, and the recovery from Covid is now basically complete.

As a reminder, ASUR operates the Cancun airport, as well as several other airports in the Southern part of Mexico, Puerto Rico’s main airport, and other airports in South America.

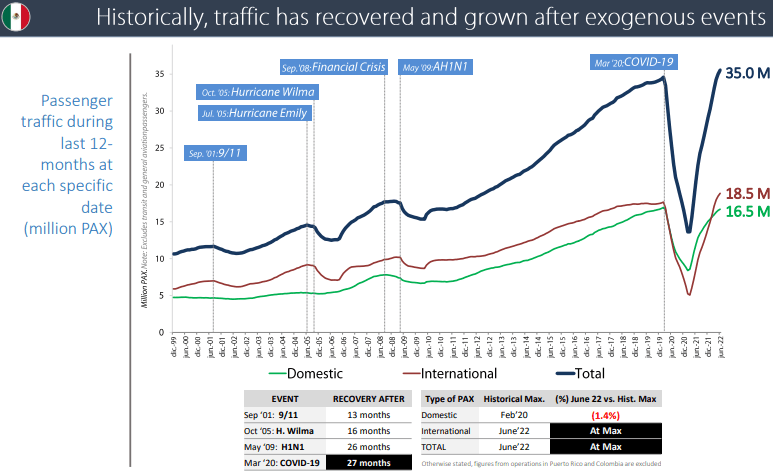

During the second quarter total traffic was up over 39% y/y, and exceeded second quarter 2019 levels by 19%, reaching a record of 16.7 million passengers in the quarter. All geographies posted sustained revenue growth with Mexico accounting for 70% of the total revenues in the quarter, Puerto Rico 17%, and Colombia 12%.

Traffic in Mexico surpassed second quarter 2019 levels by nearly 13%. With international travel up in the high teens despite higher air fares. Canada remains at 57% of the 2019 traffic levels, but this has been more than offset by strong US traffic. European tourism is just 8% below pre-pandemic levels.

ASUR reported record profitability this quarter, thanks to the effective efficiency measures and expenses controls that drove cost levels well below pre-pandemic levels, and operating leverage kicked in strongly on the traffic growth. Despite all this good news, there are still soft spots, such as business travel which is expected to continue to lag leisure and should take longer to recover.

ASUR Investor Presentation

Balance Sheet

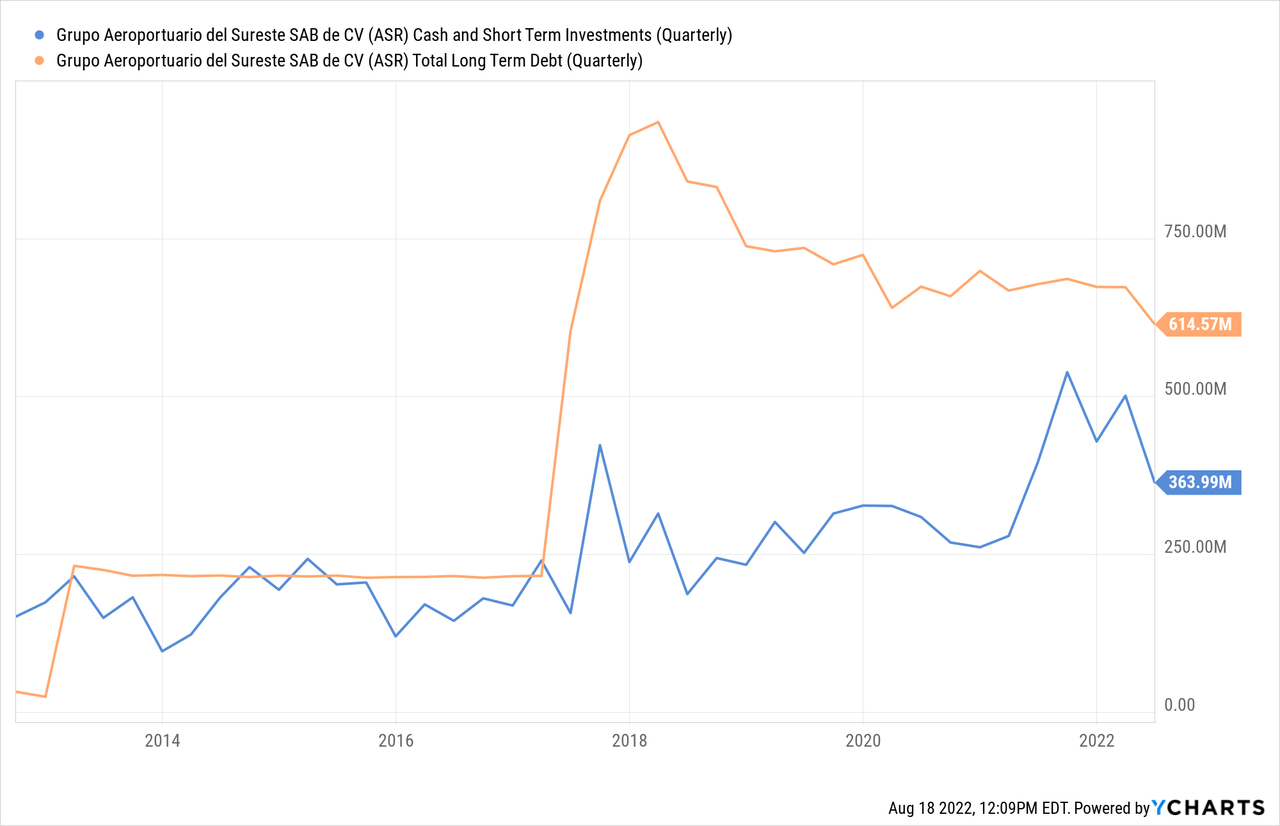

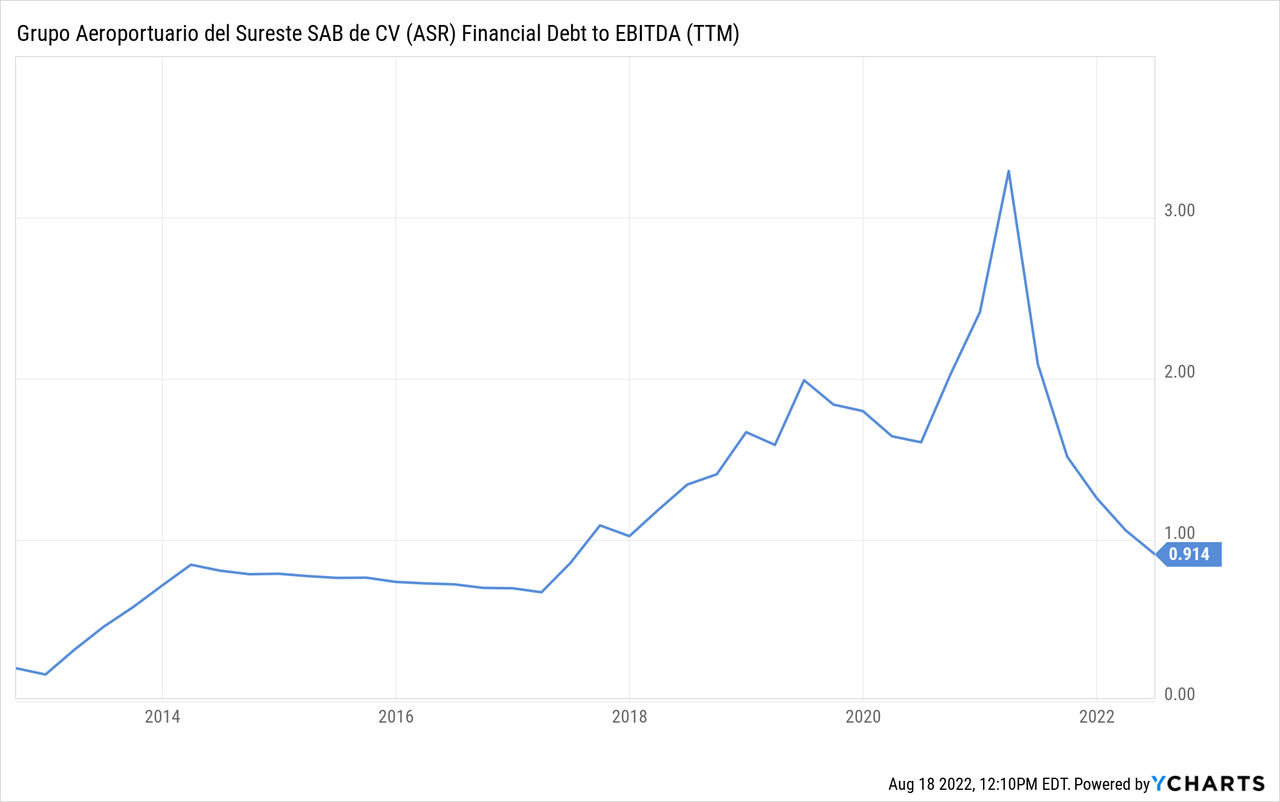

Another reason that we believe ASUR is very cheap right now is its incredibly strong balance sheet, which gives the company a lot of optionality to invest in growth and/or M&A. Net debt to EBITDA was just 0.4x at June 30, with interest coverage at 10.5 times.

If the cash position is ignored, debt to EBITDA is still very low at ~0.9x. This should give the company solid footing to invest in the business or go after new acquisitions.

Growth

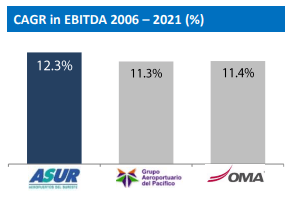

Of the three airport operator groups in Mexico, ASUR has the highest historical EBITDA growth rate. Its growth rate has been about 100bps higher compared to both Grupo Aeroportuario del Pacifico (PAC) and Grupo Aeroportuario del Centro Norte (OMAB). Still, all three business groups have delivered excellent results in our opinion.

ASUR Investor Presentation

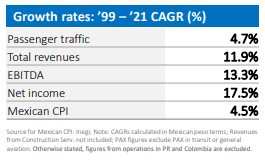

Looking at other growth metrics for ASUR, we can see that it has leveraged a 4.7% passenger traffic CAGR into an impressive Net income CAGR of ~17.5%. This compares very favorably to the Mexican inflation rate, which has averaged 4.5%. All of this to say that ASUR has been growing quickly, and that it has significant operating leverage where it can transform a relatively low increase in passenger traffic into a massive increase in earnings.

ASUR Investor Presentation

Valuation

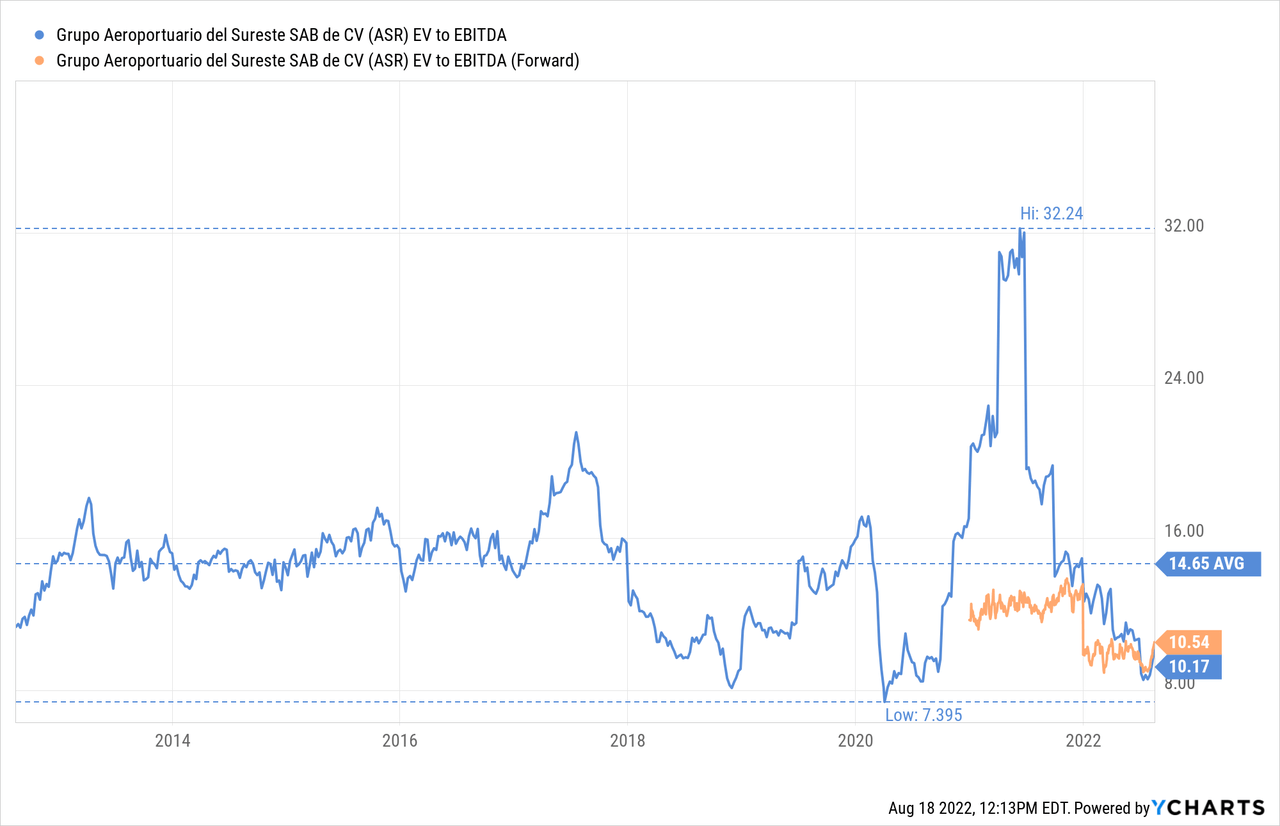

Despite the impressive recovery from Covid and the fact that the company just reported record quarterly earnings, shares continue to trade at a very reasonable valuation. The EV/EBITDA is ~10x, significantly lower than the ten year average of ~14x.

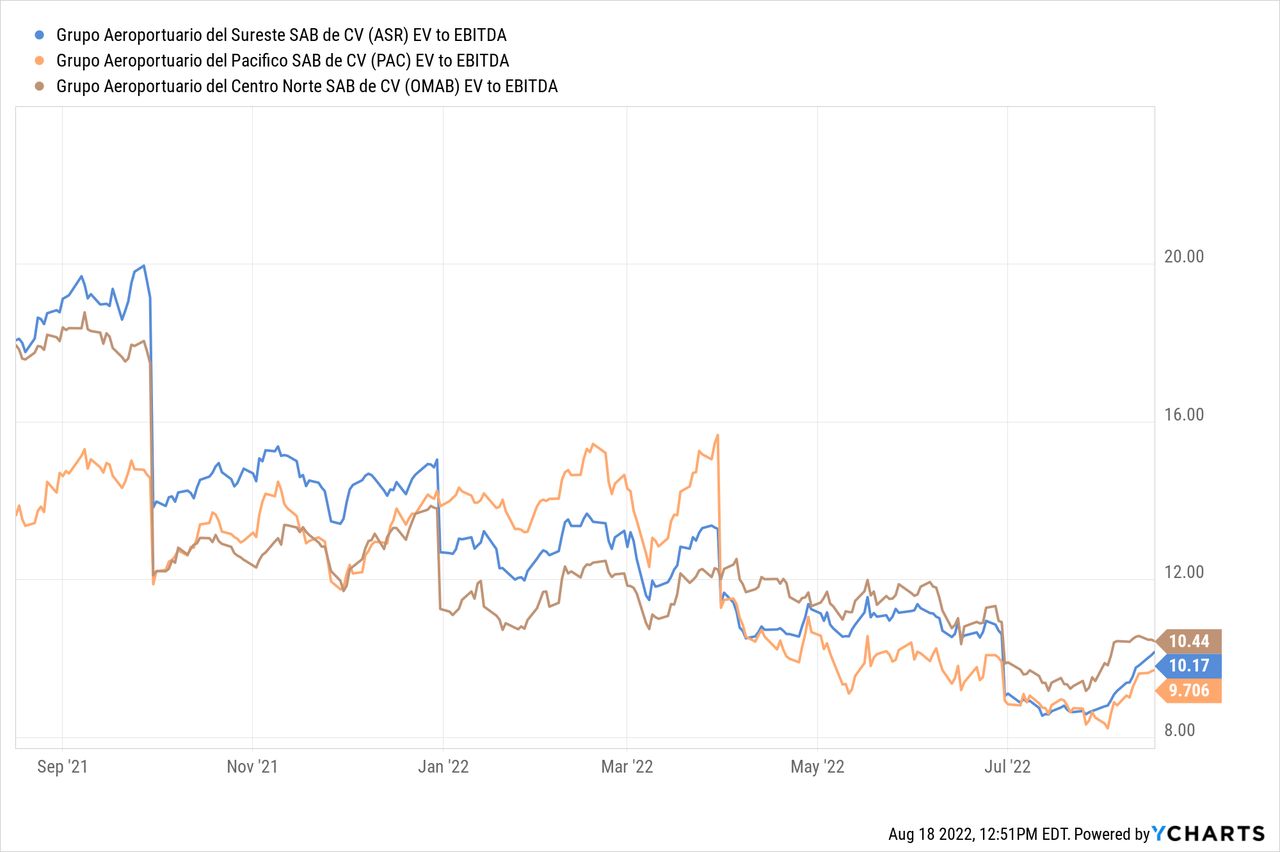

It is not only ASUR that is trading at a low valuation, PAC and OMAB are also trading with an EV/EBITDA around 10x. We like ASUR the best due to its high exposure to leisure travel, which we expect will continue outperforming business travel, as well as its higher historical EBITDA growth rate.

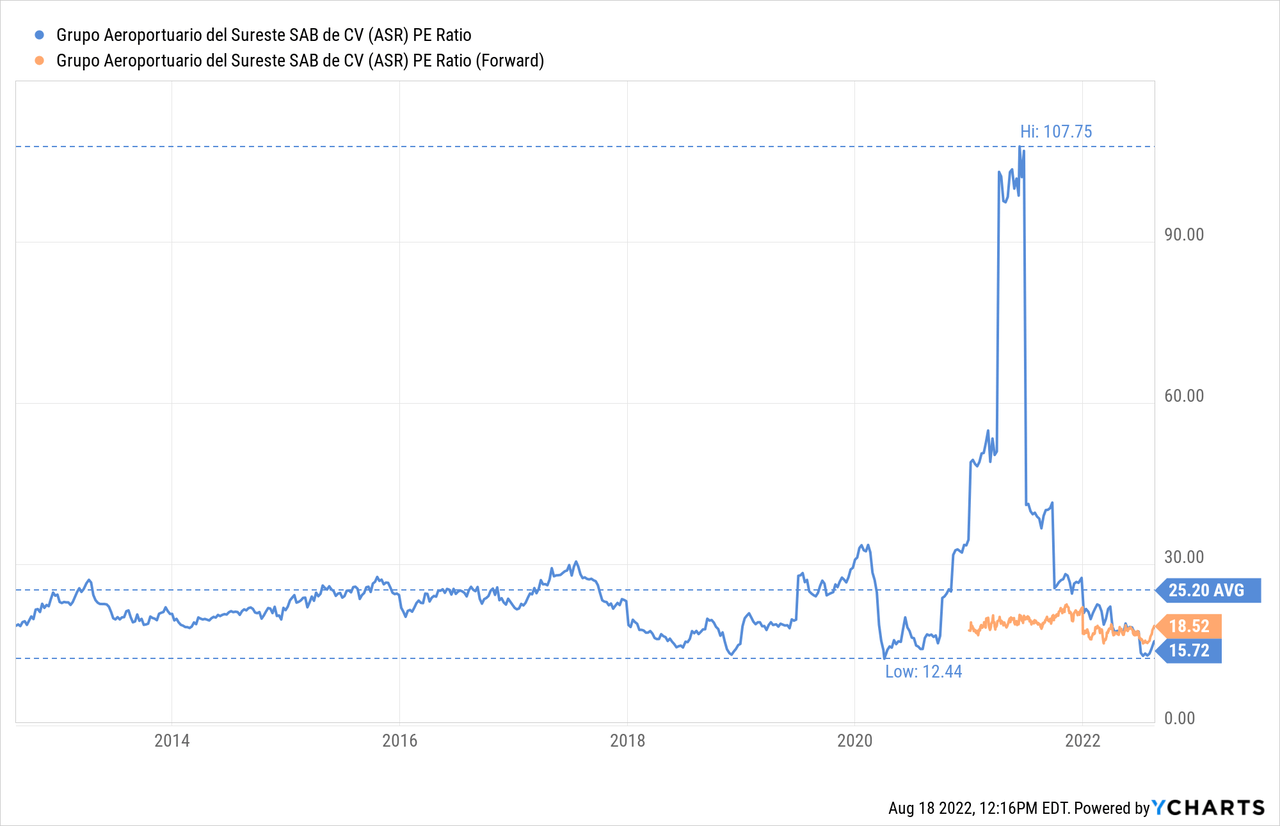

For those that prefer price/earnings to EV/EBITDA, we include that one below too. As can be seen, the current p/e ratio at ~15x is considerably below the ten year average of ~25x.

Risks

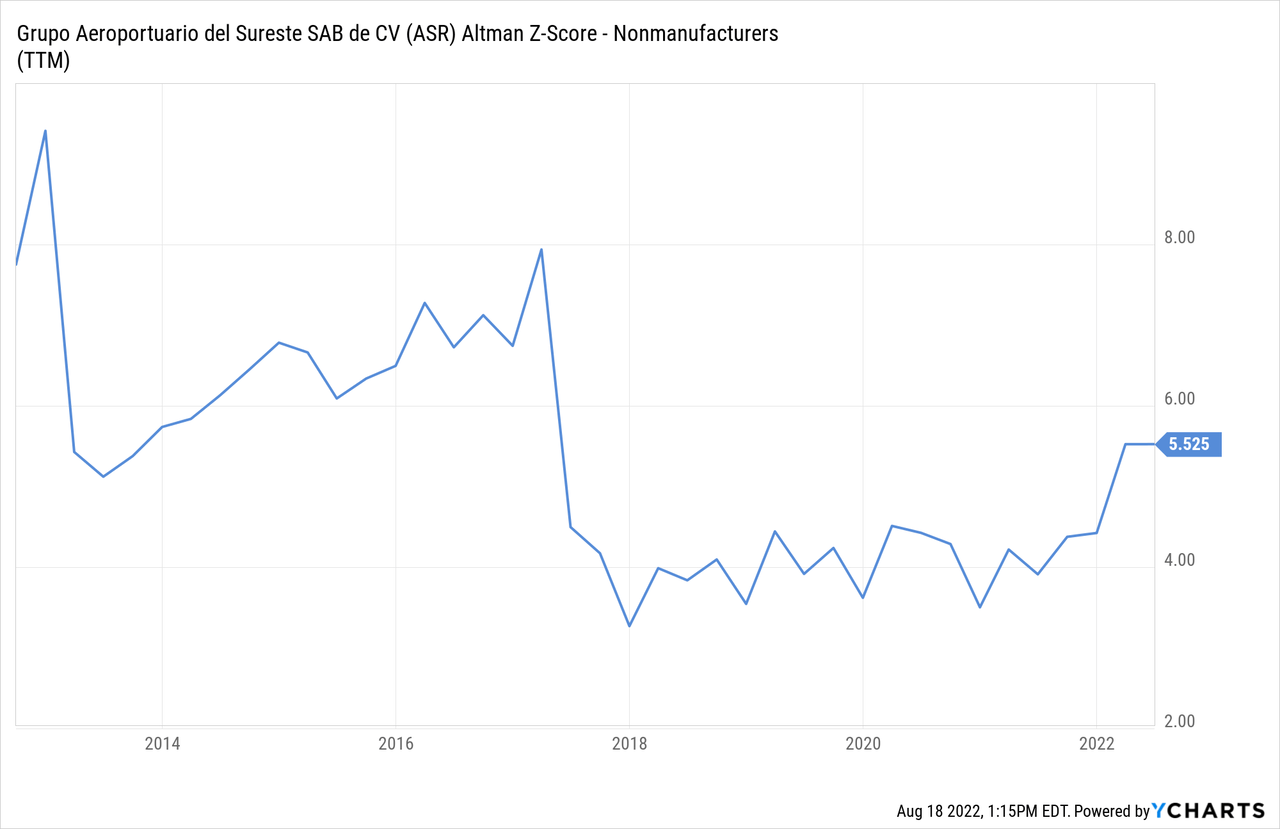

The biggest risk we see with an investment in ASUR are new travel restrictions should Covid or another disease start spreading again around the world in a significant way. To a lesser degree there is also the risk of a recession affecting travel. Fortunately the company has a very strong balance sheet, and its Altman Z-Score is considerably above the critical threshold of 3.0.

Conclusion

While shares are trading near their 52 week high, we still see a lot of value in the shares. The company has basically recovered from the Covid impact, even if there are still areas like business travel that have yet to reach pre-pandemic highs. We believe long-term investors should still take a look at the company, which has historically delivered impressive EBITDA growth, and is trading below its historical valuation average. With an EV/EBITDA of ~10x, and P/E of ~15x, we believe shares are worthy of consideration at current prices.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.