[ad_1]

Denis_Vermenko

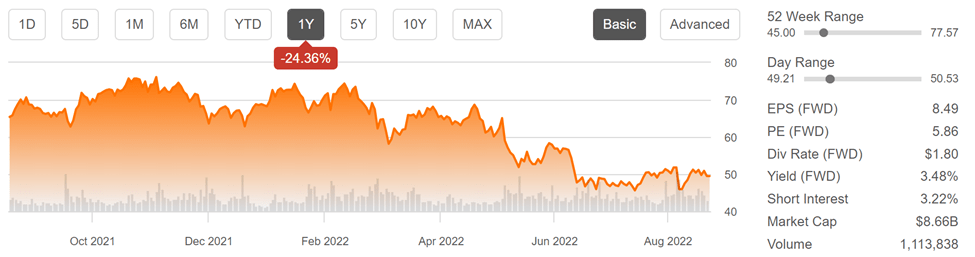

There are a number of financial stocks that remain attractively priced, especially after the market drubbing in the latter part of this week. This includes Lincoln National Corp. (NYSE:LNC), which, as seen below, has been rangebound since the middle of June and trades well below its 52-week high of $77.57. In this article, I highlight what makes this a good opportunity to layer into this quality dividend name, so let’s get started.

LNC Stock (Seeking Alpha)

Why LNC?

Lincoln National Corporation is a retirement, insurance, and wealth protection solutions provider that helps clients to address their lifestyle, savings and income goals, and guard against long-term care expenses. It’s headquartered in Pennsylvania and was founded over a century ago, in 1905. Presently, it serves 16 million customers and has $279B in total account value. Over the trailing 12 months, it generated $19.6 billion in total revenue.

LNC participates in the fast-growing U.S. markets for annuities, life insurance and workplace solutions, including group protection and retirement plan services. It also maintains a strong A- rated balance sheet with $9.6 billion of statutory surplus and an RBC (risk-based capital) ratio of 400%.

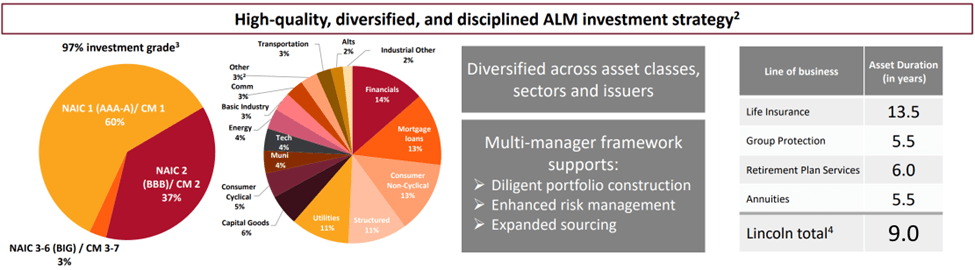

Like most insurance companies, LNC invests its insurance float (premiums not yet paid out to claimants) seeking to earn a safe and healthy return, and management follows a sound investment strategy. This is reflected by the fact that 97% of LNC’s investments are investment grade rated, and no one sector represents over 14% of the portfolio.

As shown below, the investment portfolio is well-diversified, with financials, mortgage loans, non-cyclicals, structured investments and utilities comprising 62% of the portfolio value.

LNC Investment Portfolio (Investor Presentation)

LNC is demonstrating good results, with retirement plan services having positive net inflows of $913 million during the second quarter, up $517 million from the prior year period. Moreover, life insurance sales rose by 53% YoY to $193 million, and Group Protection insurance premiums were up 7% YoY to $1.2 billion.

Also encouraging, book value per share excluding AOCI is up by 5.3% YoY to $79.49. For reference, AOCI refers to accumulated other comprehensive income that includes unrealized gains and losses reported in the equity section of the balance sheet. As such book value excluding AOCI is a more meaningful metric, especially during times of market volatility as what we witnessed during the second quarter of this year. Moreover, LNC is becoming a more efficient enterprise, as its expense ratio landed at 12.5%, down 50 basis points from Q2 of last year.

Notably, adjusted income from operations was $2.23 during Q2, down from $3.17 in the prior year period. I’m not too concerned, however, as this was driven primarily by one-time expenses, lower income from alternative investments, and equity market volatility, and not related to structural problems with the business itself. It also appears that the market has taken these results in stride, as the share price fully recovered from its drop on August 5th (day after earnings release), before declining a bit along with the market over the past couple of days.

Looking forward, LNC is targeting continued cost efficiencies in the $260-$300 million annual run-rate range through its Spark initiative, and management targets 8-10% EPS CAGR over the next few years. This could be achieved through a combination of underlying business growth as well as aggressive share repurchases.

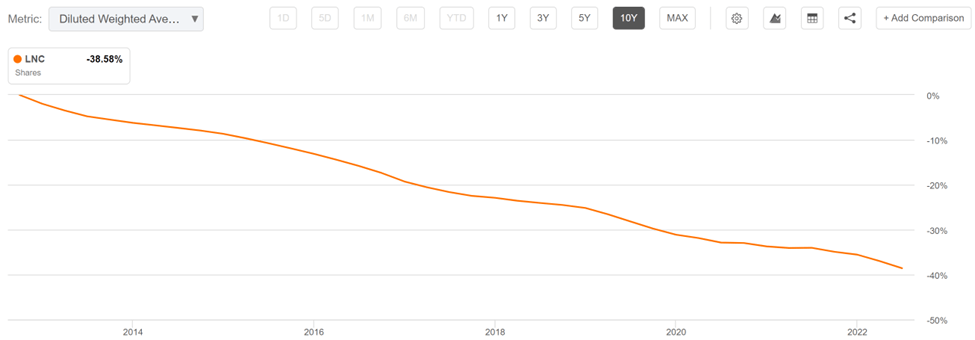

Over the past 12 months, LNC has repurchased an impressive 10% of its shares. As shown below, LNC has reduced its share count by 39% over the past 10 years.

LNC Shares Outstanding (Seeking Alpha)

Meanwhile, LNC pays a well-covered 3.6% dividend yield with a low 25% payout ratio. The dividend also has a 9.6% 5-year CAGR and 11 years of consecutive growth.

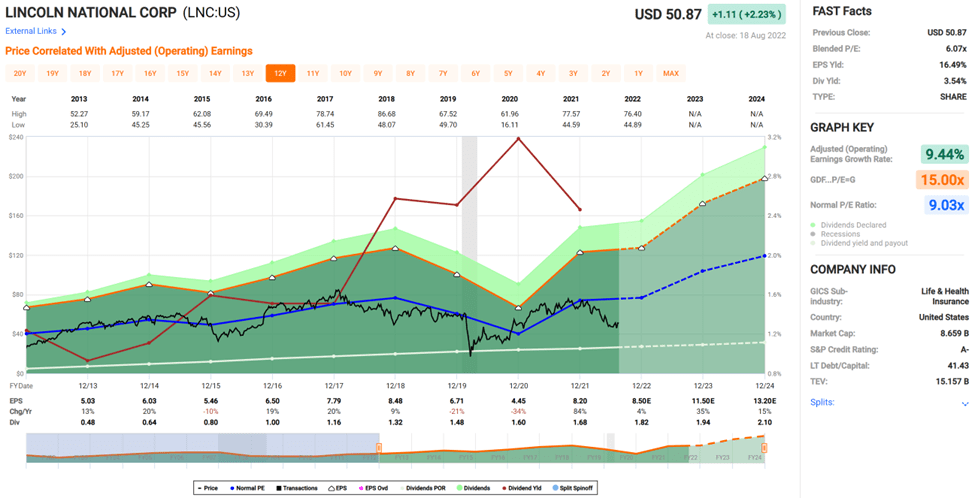

I see value in the stock at the current price of $49.47 with a forward PE of just 5.8, sitting well below its normal PE of 9.0 over the past decade. Sell side analysts have an average price target of $59.36, translating to a potential one-year 24% total return including dividends.

LNC Valuation (FAST Graphs)

Investor Takeaway

In summary, I believe LNC is a high-quality insurance company that is attractively valued at the current price. It has strong growth prospects, a well-covered dividend yield, and a history of share repurchases. The current depressed share price along with a respectable dividend yield makes LNC a sound buy for income and growth investors alike.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.