[ad_1]

Ian Tuttle

Thesis

Reflecting on the June quarter earnings season, few companies disappointed to a similar degree as online entertainment platform operator Roblox Corporation (NYSE:RBLX). The company missed analyst estimates both with regards to bookings and revenues, and the stock sold off more than 17% after the announcement (aftermarket reference). Following the June quarter results, I turn much more cautious on RBLX stock.

Since I initiated coverage on Roblox with a Buy rating and $50.3/share target price, the stock is up about 8%. While I still believe the long-term narrative of a secular growth story is attractive and remains intact, the near- to mid-term outlook looks much more challenging than what the market is pricing – and honestly more challenging than what I have expected. Accordingly, I downgrade my recommendation to Hold and adjust my target price to $45/share to reflect lower EPS outlook.

For reference, Roblox stock is down -60% versus a loss of about -15% for the S&P 500.

Seeking Alpha

Roblox’s June Quarter

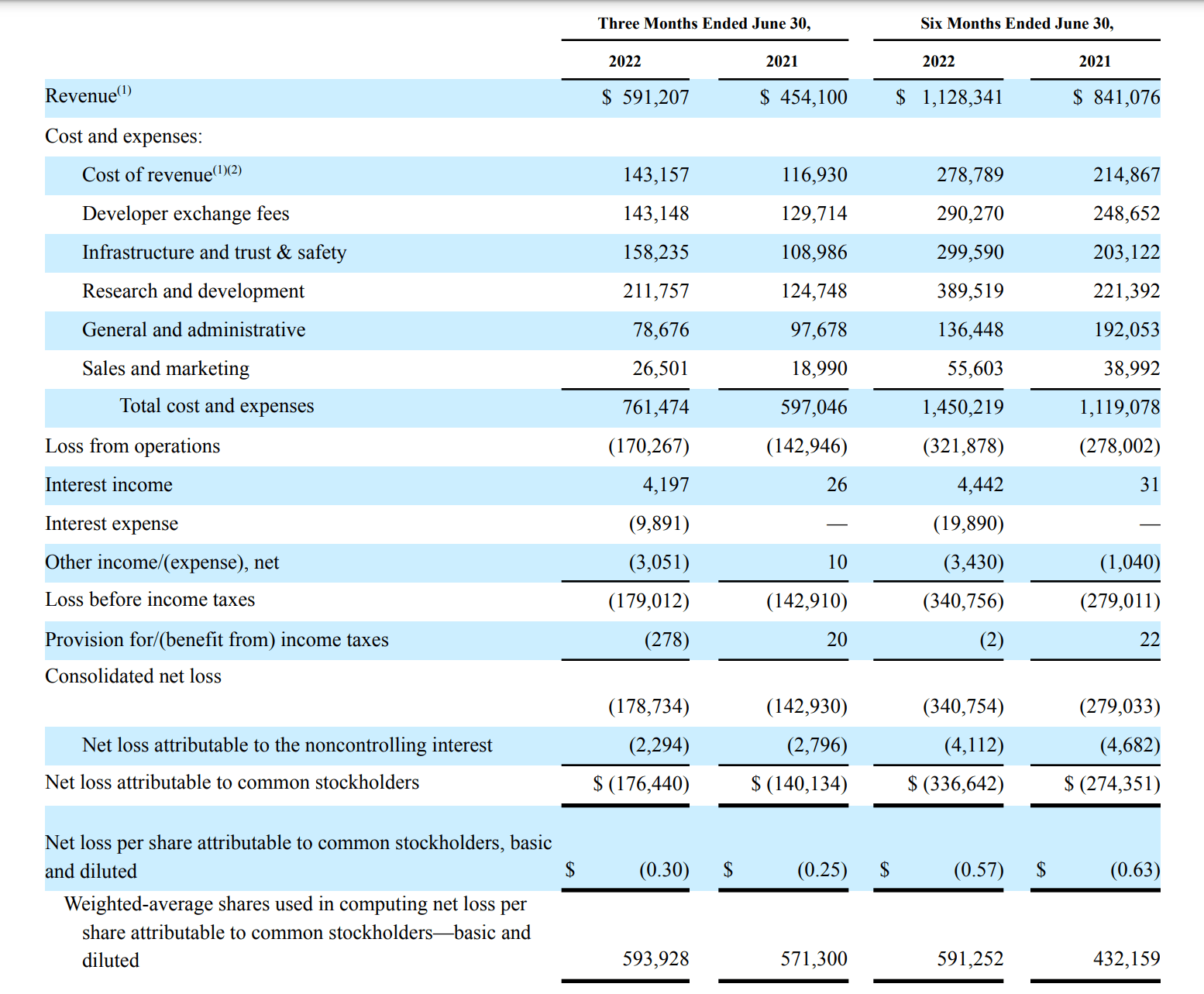

Roblox reported Q2 results on August 9th. During the period from April to end of June, the company reported revenues of $591 million (3% above consensus), which is an increase year over year of about 30%. Roblox’s net booking, however, which adjusts sales for deferred revenues and is a much more relevant metric for the company, declined by about 4% year over year to $640 million. Notably, this is the second consecutive quarter of a declining net booking metric and this does not read well for a growth stock trading at almost x10 price to sales. Roblox’s net loss was worse than expected: $176 million versus a loss of $157 million expected by analysts. Chief Business Officer Craig Donato commented on CNBC:

We’re very much in investment mode, and that’s going to put a little bit of drag on earnings, but these are investments that are the right investments for us to make that will pay off in the three-to-five-year timeframe

Roblox Q2 Results 2022

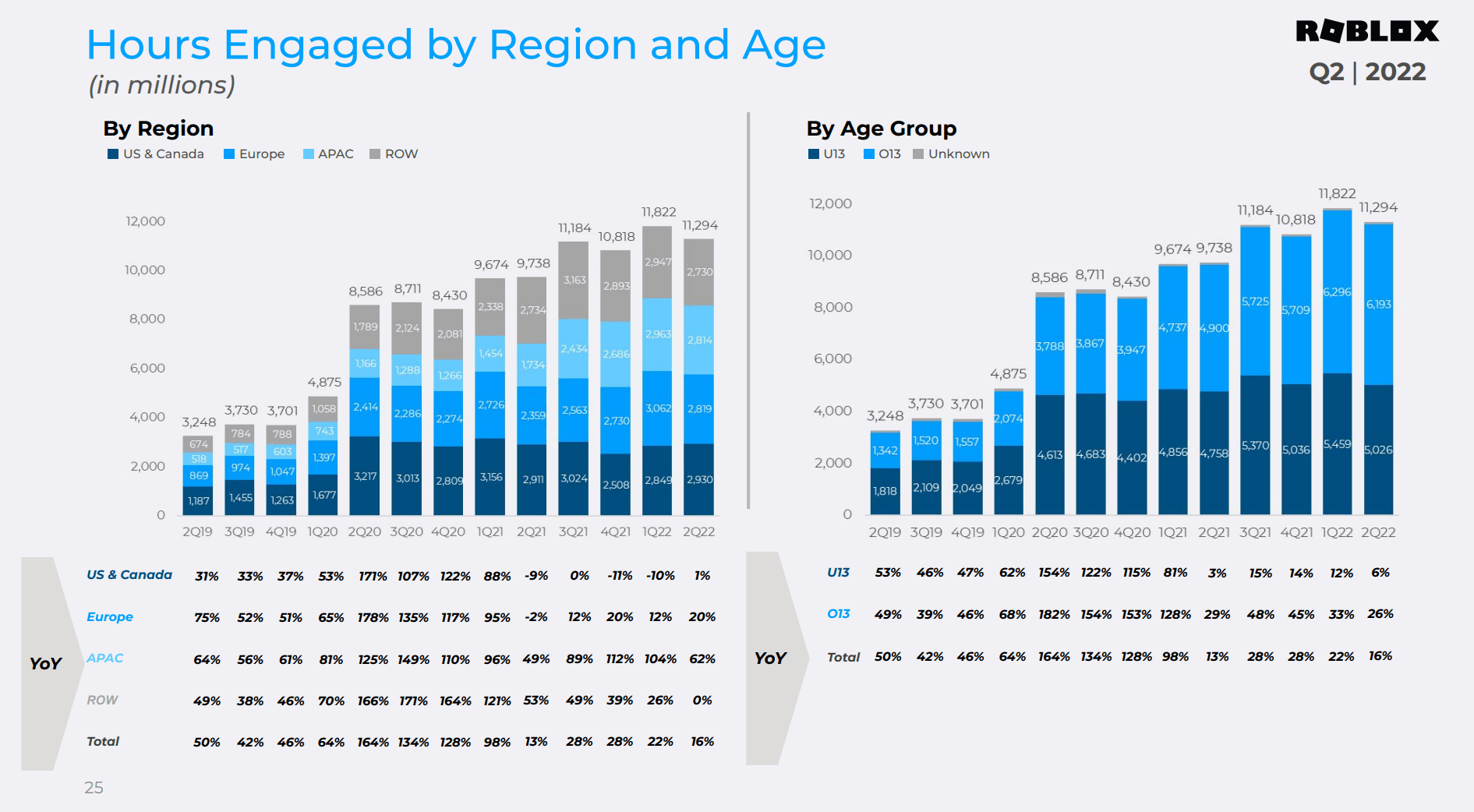

Roblox’s bad financials materialized despite strong engagement: The company reported a 21% year-over-year increase in daily active users, now being 52.2 million. Similarly, hours of engagement during the June quarter were 11.3 billion, which is a 16% increase as compared to the same period one year prior, but below consensus at 11.7 billion. That said, Roblox’s problem is connected to platform monetization, as the average net bookings per daily active user plunged by 21% to about $12.5/user.

Roblox Q2 Results 2022

Guidance

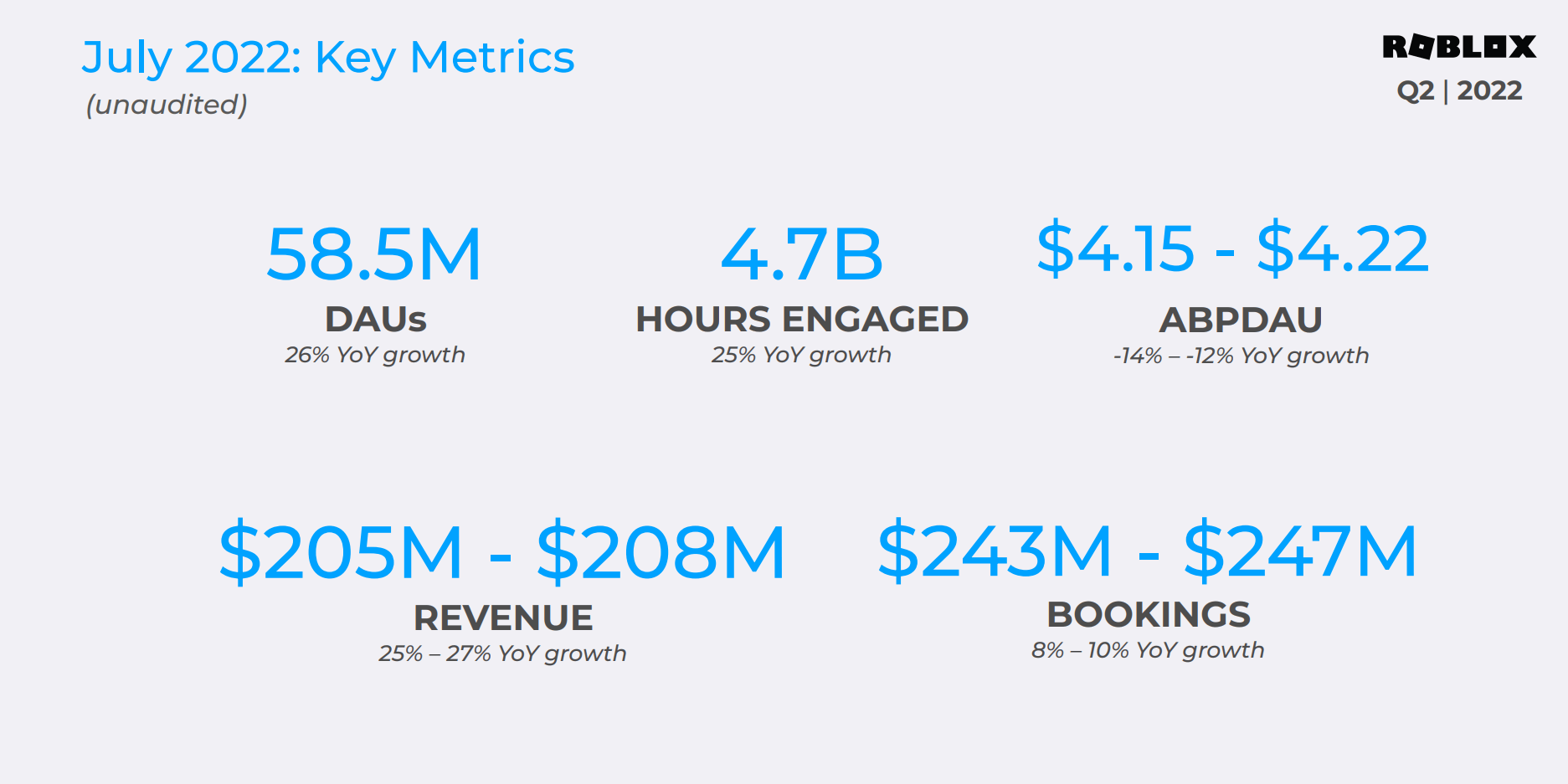

Roblox also provided some insights into the third quarter, specifically the company’s business performance during July. According to the company, daily active users achieved an absolute record of 58.5 million, which implies a 26% year-over-year growth. Bookings are estimated between $243 million and $247 million, which represents an increase of about 10% as compared to July 2021.

Roblox Investor Presentation Q2 2022

Implications

Roblox is trading at about x10 EV/Sales and x13 Price/Book. While I acknowledge Roblox’s secular growth potential connected to the metaverse narrative, I also acknowledge that the company’s valuation is incredibly stretched, leaving no room for a margin of safety. In other words, the Roblox is priced to perfection. And as the June quarter highlighted, perfection is easy to miss.

Following a very bad earnings miss, I believe investors are well advised, if they turn more cautious on the name. As we have seen, Roblox’s business performance is not immune to macroeconomic challenges and the company is clearly having trouble to ramp-up monetization, or at least grow monetization in line with engagement. Accordingly, as long as these challenges persist, I am reluctant to pay the market’s incredible valuation premium for the company’s growth potential.

Recommendation

Roblox significantly underperformed both against Q1 2021 and against analyst consensus estimates. Accordingly, I believe a more cautious investing approach is justified – one that doesn’t demand paying a x10 EV/Sales multiple.

As long as Roblox is having trouble monetizing the company’s platform in line with engagement growth, I sustain a Hold recommendation for the stock. And as compared to my previous rating, I downgrade the 12-month target price to $45/share to reflect a weaker EPS outlook.

My initiation article on Roblox: Roblox: Buy This Secular Growth Opportunity

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.