[ad_1]

lucadp

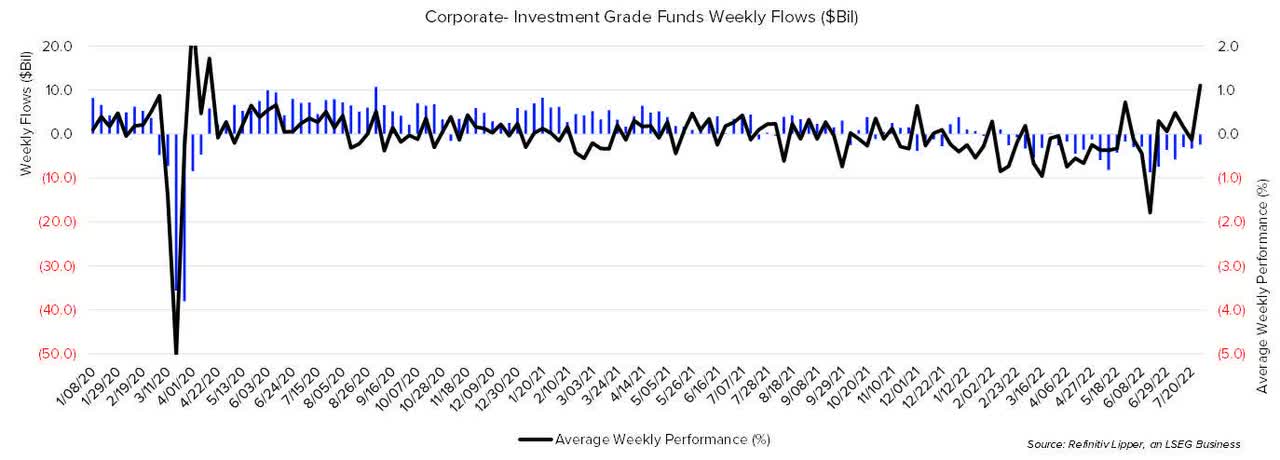

Corporate investment-grade debt funds (including both conventional mutual funds and ETFs) have suffered $113.8 billion in year-to-date outflows. This figure would already break the annual outflow record by nearly $100 billion. Investment grade (IG) corporate debt funds broke their all-time calendar year records during their 2020 and 2021 campaign (+$266.7 billion and +$274.4 billion, respectively). If the tides do not turn quickly, IG funds will only log their second calendar year outflow.

While recent performance may be trending upward, year-to-date performance has been dismal. Lipper Corporate Debt A-Rated Funds have realized a negative 11.06%, while Lipper Short Investment Grade Debt Funds and Lipper Short-Intermediate Investment Grade Debt Funds returned negative 3.54% and negative 4.50%, respectively.

Refinitiv Lipper

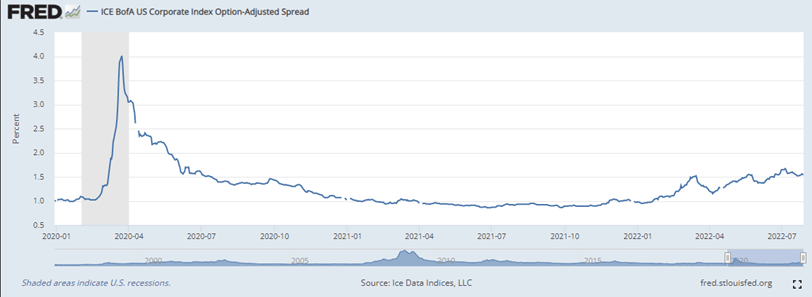

Starting after the peak pandemic, the IG Option-Adjusted Spread (OAS) tumbled to right around 100 basis points (bps). Falling spreads, easy monetary policy, and an insatiable consumer demand attracted market participants to investment grade corporate debt funds. While balance sheets looked strong in the short term, inflation and geopolitical crisis hit worldwide economies hard. To combat inflation and regain pricing control, the Federal Reserve ended its quantitative easing program while increasing interest rates at a historic pace. For the second straight month, the Fed raised the fed funds rate by at least three-quarters of a percent—it raised rates 100 bps last month for the first time since 1994.

As the monetary tightening continues, companies’ balance sheets become increasingly stressed. Just this Tuesday, Walmart (WMT) shook up the markets as shares fell by nearly 8% on an early profit warning citing inflation and supply chain challenges—also an indication that retail consumers are cutting back on spending.

Credit spreads (a.k.a. Treasury spreads) such as the ICE OAS are the difference between an index of corporate bonds and a U.S. Treasury issue with similar credit ratings and maturity dates. Credit spreads act as the additional incentive (yield) for an investor which compensates them if they choose to take on the added risk of a corporate bond rather than a “risk-free” Treasury bond. With corporate balance sheets being more strained, credit spreads have been increasing since the start of the year after remaining essentially flat during 2021. Credit spread increases, among other factors such as demand for Treasuries, have helped cause poor IG bond fund performance so far this year.

St. Louis FRED

This past fund-flows week, corporate-investment grade debt funds suffered $2.4 billion in outflows—conventional mutual funds accounted for $4.2 billion of those outflows. Corporate IG debt funds have posted 18 straight weeks of outflows, producing their second and third largest monthly outflows on record in May (-$39.1 billion) and June (-$34.6 billion). Their second quarter was the second largest quarterly outflow (-$84.1 billion), only trailing Q1 2020 (-$101.8 billion). Corporate IG debt fund’s trailing four-week outflow moving average has remained above $1.3 billion for 24 straight weeks.

This week the U.S. gross domestic product (GDP) was published at a 0.9% annualized rate during Q2 2022, which after shrinking 1.6% in Q1, translates for many market participants as an official recession. The International Monetary Fund (IMF) also lowered its global economic growth forecast this week—IMF now forecasts a 3.2% (vs. 3.6%) expansion in 2022 and a 2.9% (vs. 3.6%) expansion in 2023. If growth continues to slow with stable upward pricing pressures, we may continue to see credit spreads increase, meaning more trouble for the investment grade corporate debt bond market.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.